library(vars)

library(dplyr)

set.seed(20220725)

y1 <- rnorm(n = 31)

y2 <- y1 %>%

tail(-1) %>%

{

. * 0.7

} %>%

{

. + rnorm(30, sd = 0.1)

}

y1 <- tail(y1, -1)

y_data_VAR <- data.frame(y1, y2)Rで時系列分析:階差VARからレベルVARへの変換

Rでデータサイエンス

はじめに

- 推定用VARモデルが階差型内生変数を含む場合において、レベル型のインパルス応答値を求めたいとする。

- 内生変数の数を2つ、ラグ次数は\(\,p=1\,\)、確定項なしのモデルを例とする。

- インパルス応答値:外生的なショックに対する内生変数の変化分。

- 係数行列は\(\textbf{B}_1=\begin{bmatrix}b_{11}^1&b_{12}^1\\b_{21}^1&b_{22}^1\end{bmatrix}\)とする。

推定用内生変数ベクトルが共に階差型の場合

係数行列推定用階差VARモデル

\[\begin{bmatrix}\Delta y_{1t}\\\Delta y_{2t}\end{bmatrix}=\begin{bmatrix}b_{11}^1&b_{12}^1\\b_{21}^1&b_{22}^1\end{bmatrix}\begin{bmatrix}\Delta y_{1t-1}\\\Delta y_{2t-1}\end{bmatrix}+\begin{bmatrix}u_{1t}\\u_{2t}\end{bmatrix}\]

インパルス応答用レベルVARモデル

\[\begin{bmatrix}y_{1t}-y_{1t-1}\\ y_{2t}-y_{2t-1}\end{bmatrix}=\begin{bmatrix}b_{11}^1&b_{12}^1\\b_{21}^1&b_{22}^1\end{bmatrix}\begin{bmatrix}y_{1t-1}-y_{1t-2}\\y_{2t-1}-y_{2t-2}\end{bmatrix}+\begin{bmatrix}u_{1t}\\u_{2t}\end{bmatrix}\]

変形して、

\[\begin{bmatrix}y_{1t}\\ y_{2t}\end{bmatrix}=\begin{bmatrix}y_{1t-1}\\ y_{2t-1}\end{bmatrix}+\begin{bmatrix}b_{11}^1&b_{12}^1\\b_{21}^1&b_{22}^1\end{bmatrix}\begin{bmatrix}y_{1t-1}-y_{1t-2}\\y_{2t-1}-y_{2t-2}\end{bmatrix}+\begin{bmatrix}u_{1t}\\u_{2t}\end{bmatrix}\]

推定用内生変数ベクトルが1つはレベル、他方は階差型の場合

係数行列推定用階差VARモデル

\[\begin{bmatrix}y_{1t}\\\Delta y_{2t}\end{bmatrix}=\begin{bmatrix}b_{11}^1&b_{12}^1\\b_{21}^1&b_{22}^1\end{bmatrix}\begin{bmatrix}y_{1t-1}\\\Delta y_{2t-1}\end{bmatrix}+\begin{bmatrix}u_{1t}\\u_{2t}\end{bmatrix}\]

インパルス応答用レベルVARモデル

\[\begin{bmatrix}y_{1t}\\ y_{2t}\end{bmatrix}=\begin{bmatrix}0&0\\0&1\end{bmatrix}\begin{bmatrix}y_{1t-1}\\ y_{2t-1}\end{bmatrix}+\begin{bmatrix}b_{11}^1&b_{12}^1\\b_{21}^1&b_{22}^1\end{bmatrix}\begin{bmatrix}y_{1t-1}\\ y_{2t-1}-y_{2t-2}\end{bmatrix}+\begin{bmatrix}u_{1t}\\u_{2t}\end{bmatrix}\]

irf {vars}を利用したインパルス応答

サンプルデータ

p <- 1

out_VAR <- VAR(y = y_data_VAR, p = p, type = "none")

out_VAR %>%

summary()

VAR Estimation Results:

=========================

Endogenous variables: y1, y2

Deterministic variables: none

Sample size: 29

Log Likelihood: -6.265

Roots of the characteristic polynomial:

0.1928 0.0853

Call:

VAR(y = y_data_VAR, p = p, type = "none")

Estimation results for equation y1:

===================================

y1 = y1.l1 + y2.l1

Estimate Std. Error t value Pr(>|t|)

y1.l1 -0.5015 1.2064 -0.416 0.681

y2.l1 0.8895 1.7514 0.508 0.616

Residual standard error: 0.8449 on 27 degrees of freedom

Multiple R-Squared: 0.01955, Adjusted R-squared: -0.05307

F-statistic: 0.2692 on 2 and 27 DF, p-value: 0.766

Estimation results for equation y2:

===================================

y2 = y1.l1 + y2.l1

Estimate Std. Error t value Pr(>|t|)

y1.l1 -0.4580 0.8203 -0.558 0.581

y2.l1 0.7796 1.1908 0.655 0.518

Residual standard error: 0.5745 on 27 degrees of freedom

Multiple R-Squared: 0.0261, Adjusted R-squared: -0.04604

F-statistic: 0.3618 on 2 and 27 DF, p-value: 0.6998

Covariance matrix of residuals:

y1 y2

y1 0.7133 0.4787

y2 0.4787 0.3298

Correlation matrix of residuals:

y1 y2

y1 1.000 0.987

y2 0.987 1.000# 係数行列 B1

Bcoef(x = out_VAR) y1.l1 y2.l1

y1 -0.5015106 0.8894964

y2 -0.4580417 0.7796057インパルス応答の累積値

- 引数「cumulative」をTRUEとする。

- 恒久的な波及効果

irf(x = out_VAR, impulse = "y1", response = "y2", n.ahead = 20, ortho = F, boot = F, cumulative = T) %>%

plot()

irf(x = out_VAR, impulse = "y2", response = "y1", n.ahead = 20, ortho = F, boot = F, cumulative = T) %>%

plot()

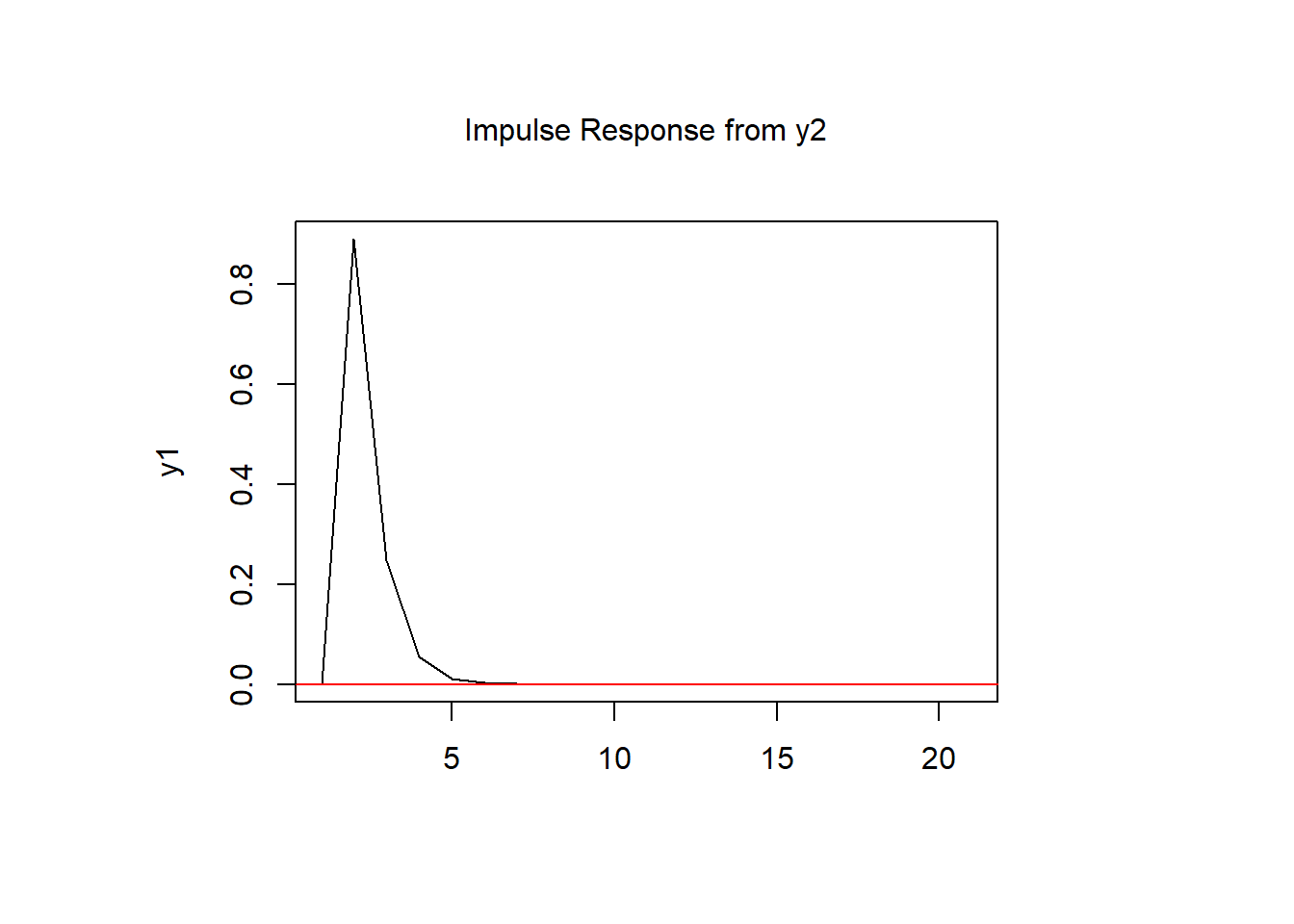

インパルス応答の非累積値

- 引数「cumulative」をFALSEとする。

- ゼロに収束する過渡的な波及効果。

irf(x = out_VAR, impulse = "y1", response = "y2", n.ahead = 20, ortho = F, boot = F, cumulative = F) %>%

plot()

irf(x = out_VAR, impulse = "y2", response = "y1", n.ahead = 20, ortho = F, boot = F, cumulative = F) %>%

plot()

参照引用資料

- 村尾博(2019),『Rで学ぶVAR実証分析』,オーム社,pp.288-293

最終更新

Sys.time()[1] "2024-04-16 10:13:16 JST"R、Quarto、Package

R.Version()$version.string[1] "R version 4.3.3 (2024-02-29 ucrt)"quarto::quarto_version()[1] '1.4.553'packageVersion(pkg = "tidyverse")[1] '2.0.0'