library(seasonal)

packageVersion("seasonal")[1] '1.9.0'Rでデータサイエンス

library(seasonal)

packageVersion("seasonal")[1] '1.9.0'rbind(head(df_iip), tail(df_iip)) date IIP_NSA IIP_SA

1 2018-01-01 105.6 112.3

2 2018-02-01 111.0 114.6

3 2018-03-01 128.1 116.3

4 2018-04-01 111.8 114.5

5 2018-05-01 109.9 115.1

6 2018-06-01 115.5 114.3

67 2023-07-01 105.1 103.5

68 2023-08-01 96.1 103.1

69 2023-09-01 107.0 103.2

70 2023-10-01 106.3 104.4

71 2023-11-01 106.9 103.8

72 2023-12-01 106.4 105.0df_iip %>%

gather(key = "IIP", value = "value", colnames(.)[-1]) %>%

ggplot(mapping = aes(x = date, y = value, col = IIP)) + geom_point() + geom_line()

# ts class に変換

(iip_nsa <- df_iip$IIP_NSA %>%

ts(start = df_iip$date %>%

head(1) %>%

{

c(year(.), month(.))

}, end = df_iip$date %>%

tail(1) %>%

{

c(year(.), month(.))

}, frequency = 12)) Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2018 105.6 111.0 128.1 111.8 109.9 115.5 117.0 108.0 113.8 120.2 119.0 115.7

2019 106.0 110.4 122.9 111.4 107.9 111.9 118.2 102.6 115.9 110.8 109.7 111.4

2020 102.7 103.7 116.5 94.8 80.0 91.6 99.1 87.9 104.6 106.2 104.8 107.9

2021 97.4 101.4 120.1 108.4 95.4 111.6 109.9 95.4 103.1 102.2 110.1 110.0

2022 96.7 101.4 118.2 103.3 92.8 108.3 107.9 100.8 112.1 105.4 108.6 107.6

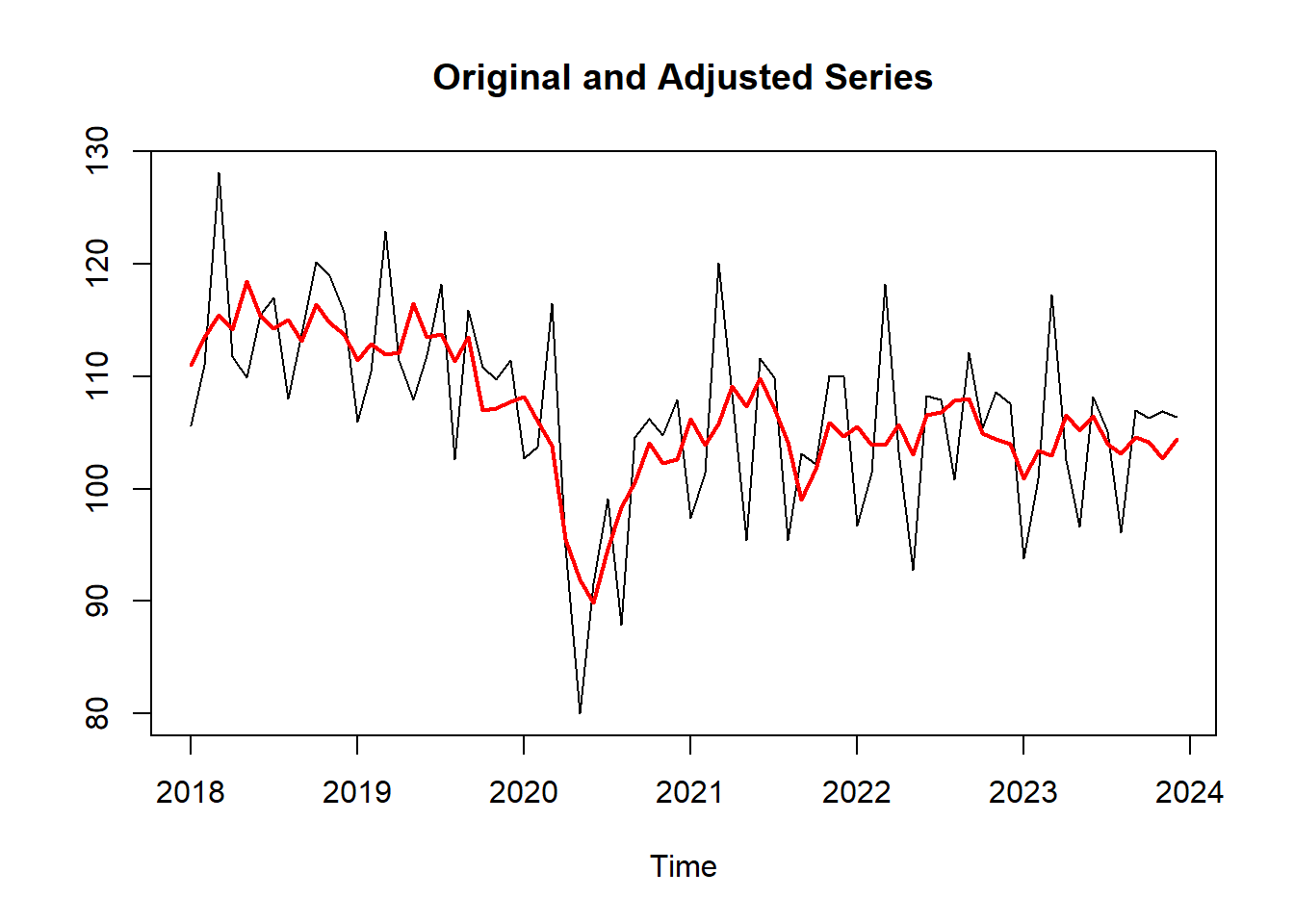

2023 93.8 100.9 117.3 102.5 96.6 108.2 105.1 96.1 107.0 106.3 106.9 106.4sa <- seas(x = iip_nsa)

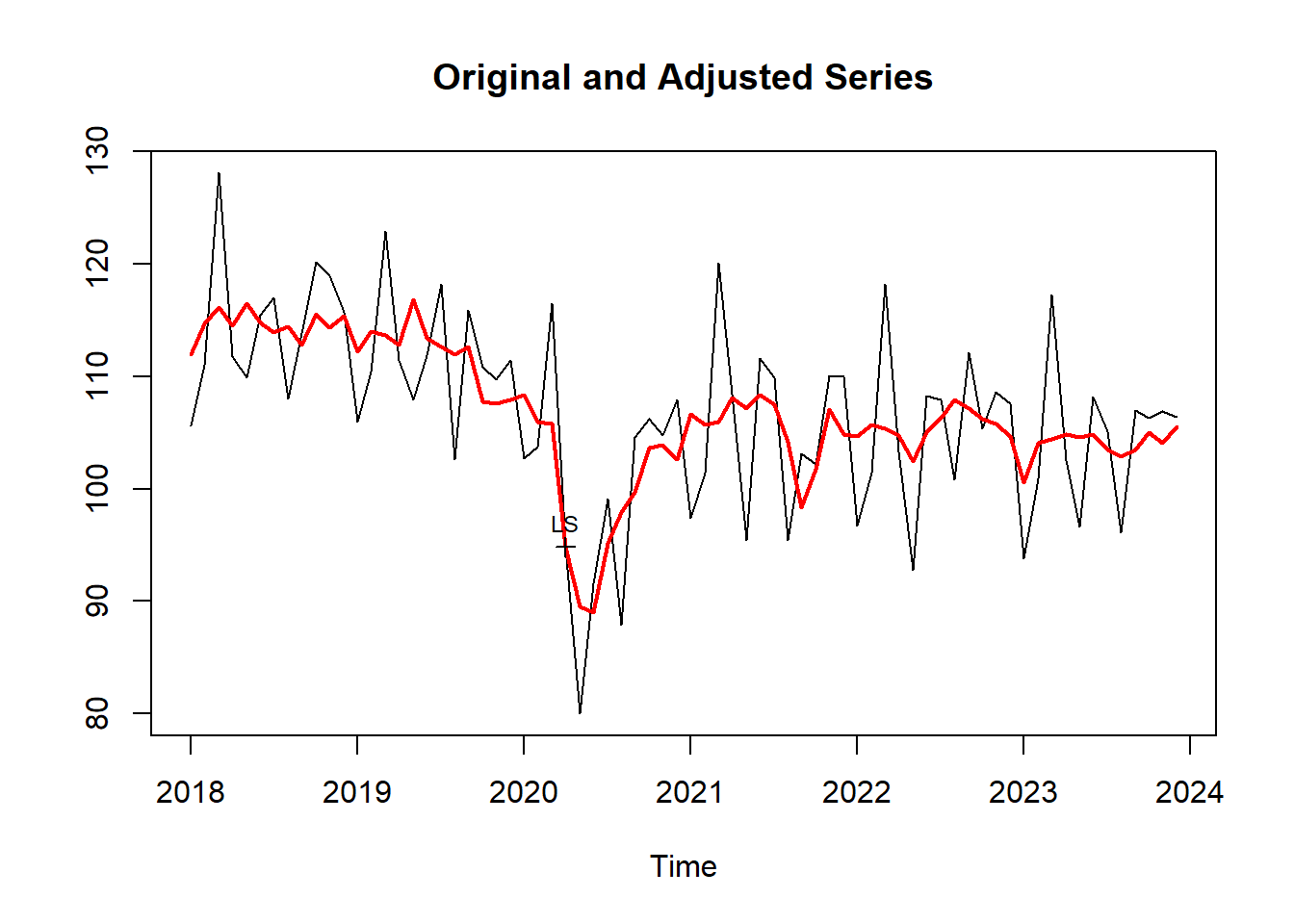

sa %>%

plot()

デフォルトの季節調整はSEATSが選択される。

summary(sa)

Call:

seas(x = iip_nsa)

Coefficients:

Estimate Std. Error z value Pr(>|z|)

Leap Year 1.3553 2.2302 0.608 0.5434

Weekday 0.4795 0.0707 6.783 0.0000000000118 ***

AR-Nonseasonal-01 0.7637 0.1694 4.507 0.0000065622008 ***

AR-Nonseasonal-02 0.1497 0.1352 1.108 0.2680

AR-Nonseasonal-03 -0.2200 0.1111 -1.980 0.0477 *

MA-Nonseasonal-01 0.8411 0.1498 5.615 0.0000000196736 ***

MA-Seasonal-12 0.9872 0.1184 8.339 < 0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

SEATS adj. ARIMA: (3 1 1)(0 1 1) Obs.: 72 Transform: none

AICc: 329.5, BIC: 343.3 QS (no seasonality in final):0.00426

Box-Ljung (no autocorr.): 31.82 Shapiro (normality): 0.9709 .sa$modelregression{

variables = td1coef

b = (1.355331048 0.4795307604)

}

arima{

model = (3 1 1)(0 1 1)

ar = (0.7636725326 0.1497353889 -0.2200031053)

ma = (0.8411102719 0.9872440861)

} sa$fivebestmdl[1:8] %>%

paste0(collapse = "") %>%

paste0("</p>") %>%

cat()Best Five ARIMA Models

Model # 1 : (1 0 0)(0 1 1) (BIC2 = 5.483)

Model # 2 : (2 0 0)(0 1 1) (BIC2 = 5.551)

Model # 3 : (1 0 1)(0 1 1) (BIC2 = 5.551)

Model # 4 : (1 0 2)(0 1 1) (BIC2 = 5.569)

Model # 5 : (2 0 1)(0 1 1) (BIC2 = 5.618)

sa <- seas(x = iip_nsa, arima.model = "(1 0 0)(0 1 1)")

summary(sa)

Call:

seas(x = iip_nsa, arima.model = "(1 0 0)(0 1 1)")

Coefficients:

Estimate Std. Error z value Pr(>|z|)

Leap Year 1.39985 2.29569 0.610 0.542

Weekday 0.48286 0.07753 6.228 0.000000000472239299 ***

AR-Nonseasonal-01 0.89610 0.05002 17.913 < 0.0000000000000002 ***

MA-Seasonal-12 0.87881 0.10720 8.198 0.000000000000000244 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

SEATS adj. ARIMA: (1 0 0)(0 1 1) Obs.: 72 Transform: none

AICc: 327.8, BIC: 337.2 QS (no seasonality in final): 0

Box-Ljung (no autocorr.): 37.03 * Shapiro (normality): 0.974 sa$modelregression{

variables = td1coef

b = (1.399845881 0.4828605803)

}

arima{

model = (1 0 0)(0 1 1)

ar = 0.8960968219

ma = 0.8788061537

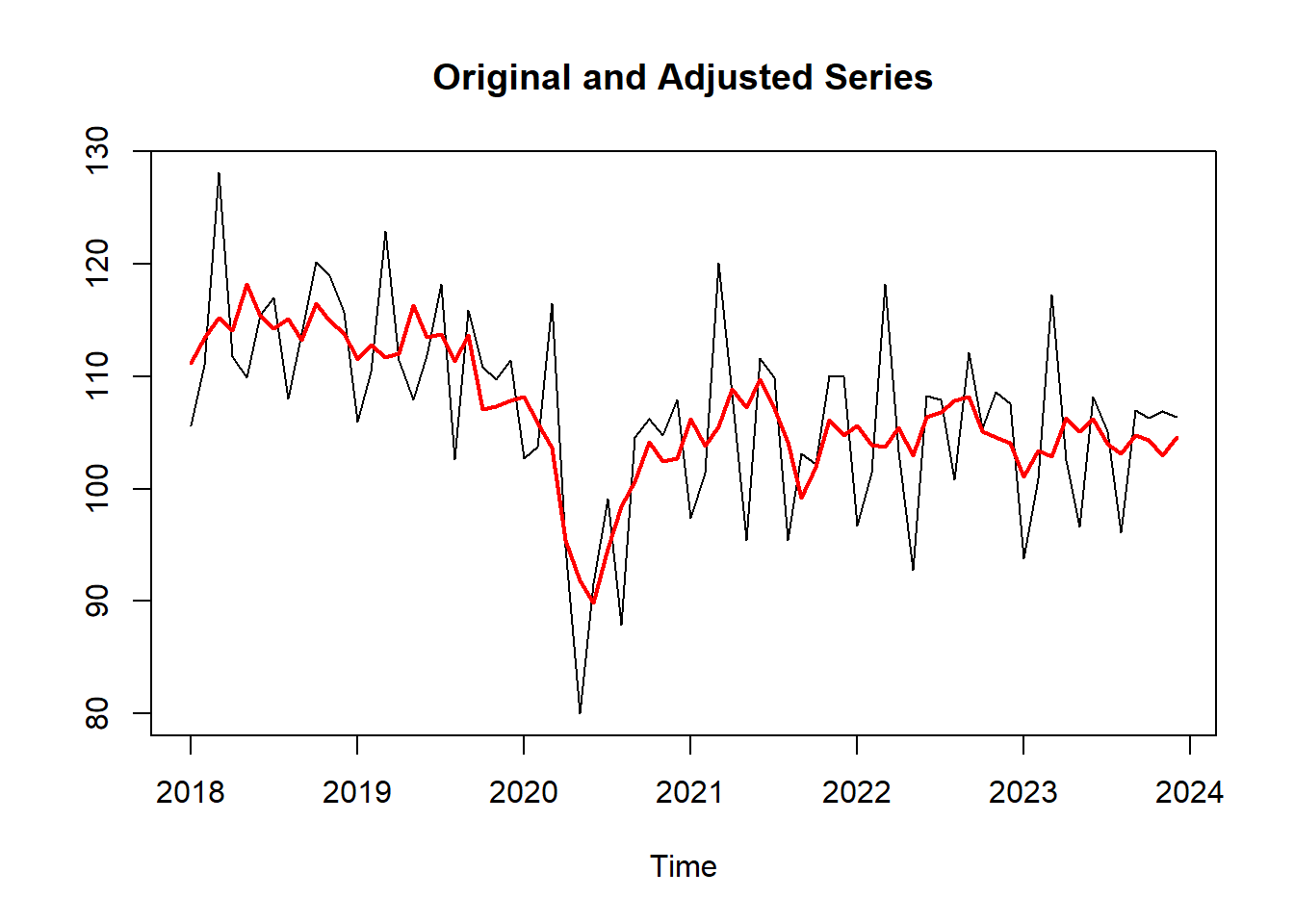

} plot(sa)

data.frame(sa) %>%

tail() date final seasonal seasonaladj trend irregular adjustfac

67 2023-07-01 103.9833 3.048095 103.9833 104.3520 -0.3686180 1.116653

68 2023-08-01 103.1740 -8.522564 103.1740 103.7715 -0.5975525 -7.073982

69 2023-09-01 104.7198 3.004471 104.7198 104.2382 0.4816573 2.280180

70 2023-10-01 104.3146 2.226830 104.3146 104.0793 0.2353180 1.985400

71 2023-11-01 102.9407 2.993601 102.9407 103.7056 -0.7649685 3.959322

72 2023-12-01 104.5916 3.739810 104.5916 104.2091 0.3824838 1.808367df_result <- data.frame(sa)[, c("date", "final")] %>%

join(df_iip[, c("date", "IIP_SA")], .)

df_result %>%

gather(key = "series", value = "value", colnames(.)[-1]) %>%

ggplot(mapping = aes(x = date, y = value, col = series)) + geom_line() + geom_point()

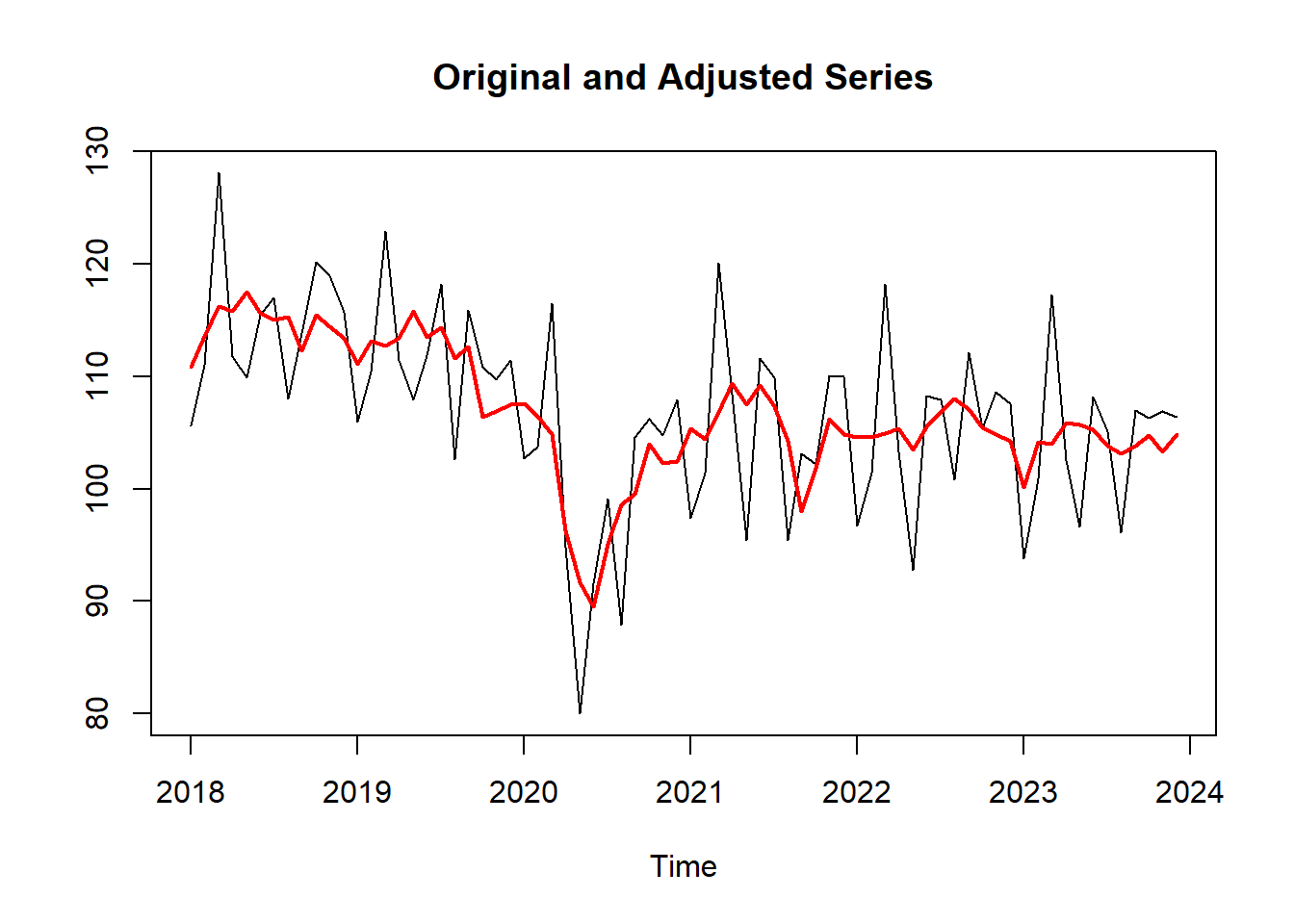

sa <- seas(x = iip_nsa, x11 = "")

sa %>%

plot()

summary(sa)

Call:

seas(x = iip_nsa, x11 = "")

Coefficients:

Estimate Std. Error z value Pr(>|z|)

Leap Year 1.3553 2.2302 0.608 0.5434

Weekday 0.4795 0.0707 6.783 0.0000000000118 ***

AR-Nonseasonal-01 0.7637 0.1694 4.507 0.0000065622008 ***

AR-Nonseasonal-02 0.1497 0.1352 1.108 0.2680

AR-Nonseasonal-03 -0.2200 0.1111 -1.980 0.0477 *

MA-Nonseasonal-01 0.8411 0.1498 5.615 0.0000000196736 ***

MA-Seasonal-12 0.9872 0.1184 8.339 < 0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

X11 adj. ARIMA: (3 1 1)(0 1 1) Obs.: 72 Transform: none

AICc: 329.5, BIC: 343.3 QS (no seasonality in final): 0

Box-Ljung (no autocorr.): 31.82 Shapiro (normality): 0.9709 .sa$modelregression{

variables = td1coef

b = (1.355331048 0.4795307604)

}

arima{

model = (3 1 1)(0 1 1)

ar = (0.7636725326 0.1497353889 -0.2200031053)

ma = (0.8411102719 0.9872440861)

} sa$fivebestmdl[1:8] %>%

paste0(collapse = "") %>%

paste0("</p>") %>%

cat()Best Five ARIMA Models

Model # 1 : (1 0 0)(0 1 1) (BIC2 = 5.483)

Model # 2 : (2 0 0)(0 1 1) (BIC2 = 5.551)

Model # 3 : (1 0 1)(0 1 1) (BIC2 = 5.551)

Model # 4 : (1 0 2)(0 1 1) (BIC2 = 5.569)

Model # 5 : (2 0 1)(0 1 1) (BIC2 = 5.618)

sa <- seas(x = iip_nsa, x11 = "", arima.model = "(1 0 0)(0 1 1)")

summary(sa)

Call:

seas(x = iip_nsa, x11 = "", arima.model = "(1 0 0)(0 1 1)")

Coefficients:

Estimate Std. Error z value Pr(>|z|)

Leap Year 1.39985 2.29569 0.610 0.542

Weekday 0.48286 0.07753 6.228 0.000000000472239299 ***

AR-Nonseasonal-01 0.89610 0.05002 17.913 < 0.0000000000000002 ***

MA-Seasonal-12 0.87881 0.10720 8.198 0.000000000000000244 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

X11 adj. ARIMA: (1 0 0)(0 1 1) Obs.: 72 Transform: none

AICc: 327.8, BIC: 337.2 QS (no seasonality in final): 0

Box-Ljung (no autocorr.): 37.03 * Shapiro (normality): 0.974 sa$modelregression{

variables = td1coef

b = (1.399845881 0.4828605803)

}

arima{

model = (1 0 0)(0 1 1)

ar = 0.8960968219

ma = 0.8788061537

} sa_seats <- seas(x = iip_nsa, arima.model = "(1 0 0)(0 1 1)") %>%

data.frame() %>%

{

.[, c("date", "final")]

} %>%

{

.$MA <- "SEATS"

.

}

sa_x11 <- seas(x = iip_nsa, arima.model = "(1 0 0)(0 1 1)", x11 = "", ) %>%

data.frame() %>%

{

.[, c("date", "final")]

} %>%

{

.$MA <- "X11"

.

}

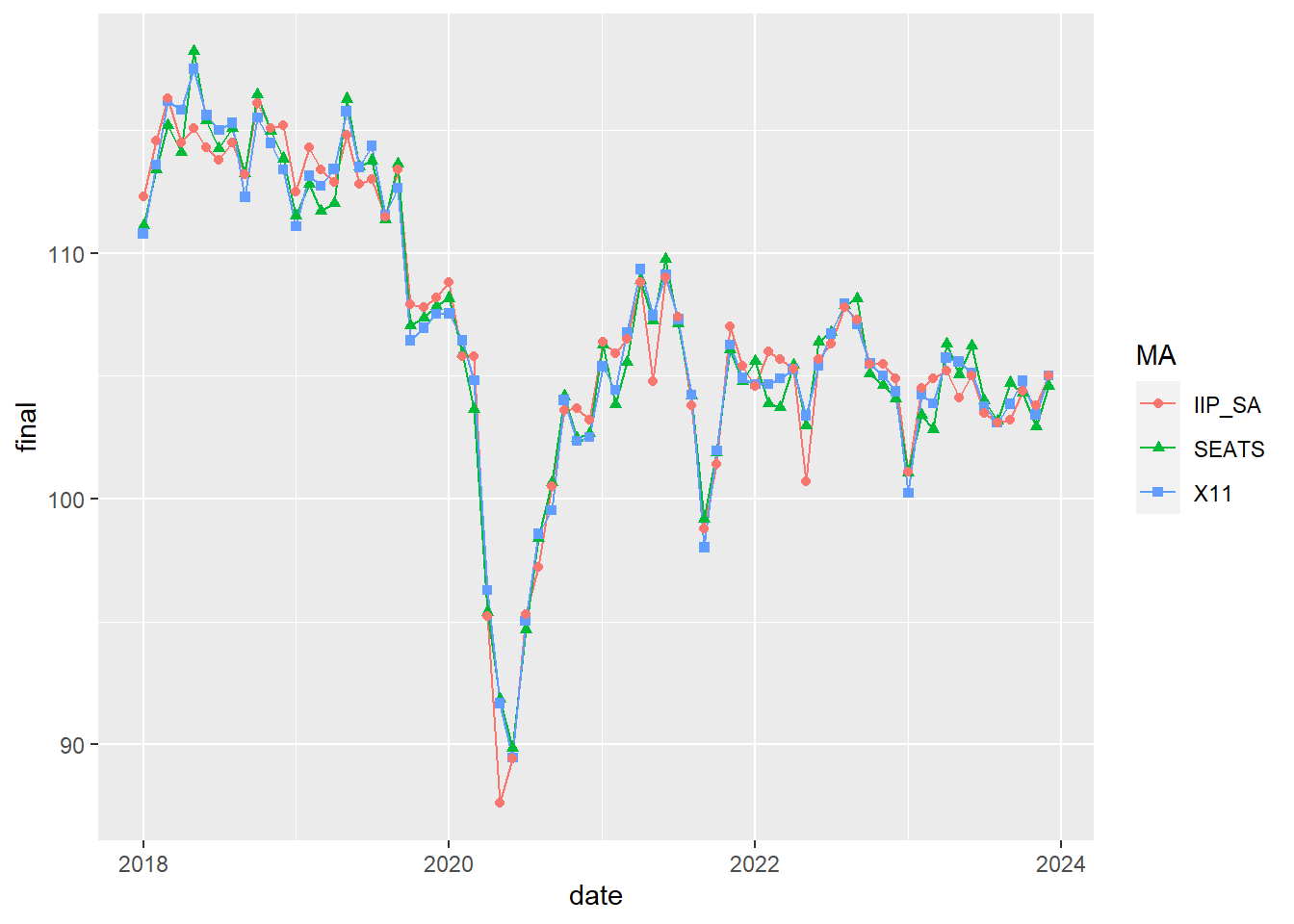

sa_iip <- df_iip[, c("date", "IIP_SA")] %>%

{

.$MA <- "IIP_SA"

colnames(.)[2] <- "final"

.

}

Reduce(function(x, y) rbind(x, y), list(sa_seats, sa_x11, sa_iip)) %>%

ggplot(mapping = aes(x = date, y = final, col = MA, shape = MA)) + geom_line() + geom_point()

回帰変数に lpyear のみを指定すると以下のエラーメッセージが表示される。なお、エラーメッセージ中の for の後にはspcファイルのパス(Tempフォルダ)が続く。

seas(x = iip_nsa, regression.variables = "lpyear")Error: X-13 run failed

Errors:

- Leap Year is already in the regression. Program error(s) halt execution for

祝祭日調整に用いる祝日変数の作成方法については、以下のとおり。

xreg_holiday Jan Feb Mar Apr May Jun Jul Aug Sep Oct

2011 -0.833 -0.083 0.167 0.000 0.250 0.000 -0.167 -0.500 0.083 0.083

2012 0.167 -1.083 0.167 0.000 -0.750 0.000 -0.167 -0.500 -0.917 0.083

2013 0.167 -0.083 0.167 0.000 -0.750 0.000 -0.167 -0.500 0.083 0.083

2014 0.167 -0.083 0.167 0.000 -0.750 0.000 -0.167 -0.500 0.083 0.083

2015 0.167 -0.083 -0.833 0.000 0.250 0.000 -0.167 -0.500 1.083 0.083

2016 0.167 -0.083 0.167 0.000 0.250 0.000 -0.167 0.500 0.083 0.083

2017 0.167 -1.083 0.167 -1.000 0.250 0.000 -0.167 0.500 -0.917 0.083

2018 0.167 -0.083 0.167 0.000 -0.750 0.000 -0.167 -0.500 0.083 0.083

2019 0.167 -0.083 0.167 1.000 1.250 0.000 -0.167 0.500 0.083 1.083

2020 0.167 0.917 0.167 0.000 0.250 0.000 0.833 0.500 0.083 -0.917

2021 0.167 0.917 -0.833 0.000 0.250 0.000 0.833 0.500 0.083 -0.917

2022 -0.833 0.917 0.167 0.000 0.250 0.000 -0.167 0.500 0.083 0.083

2023 0.167 -0.083 0.167 -1.000 0.250 0.000 -0.167 0.500 -0.917 0.083

2024 0.167 0.917 0.167 0.000 -0.750 0.000 -0.167 0.500 0.083 0.083

Nov Dec

2011 0.333 0.417

2012 -0.667 0.417

2013 -0.667 0.417

2014 0.333 0.417

2015 0.333 0.417

2016 0.333 0.417

2017 0.333 -0.583

2018 -0.667 0.417

2019 -0.667 -0.583

2020 0.333 -0.583

2021 0.333 -0.583

2022 0.333 -0.583

2023 0.333 -0.583

2024 -0.667 -0.583sa_x11_holiday <- seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", xreg = xreg_holiday, regression.usertype = "holiday")sa_x11_holiday %>%

plot()

summary(sa_x11_holiday)

Call:

seas(x = iip_nsa, xreg = xreg_holiday, transform.function = "log",

x11 = "", x11.mode = "mult", regression.usertype = "holiday")

Coefficients:

Estimate Std. Error z value Pr(>|z|)

xreg -0.0097753 0.0046864 -2.086 0.037 *

Weekday 0.0056723 0.0007199 7.879 0.00000000000000329 ***

LS2020.Apr -0.1206140 0.0269014 -4.484 0.00000734116067634 ***

MA-Nonseasonal-01 0.1526222 0.1069457 1.427 0.154

MA-Seasonal-12 0.9988016 0.1266074 7.889 0.00000000000000305 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

X11 adj. ARIMA: (0 1 1)(0 1 1) Obs.: 72 Transform: log

AICc: 314.8, BIC: 325.6 QS (no seasonality in final):0.03806

Box-Ljung (no autocorr.): 44.09 ** Shapiro (normality): 0.9854 sa_x11_holiday$modelregression{

variables = (td1coef ls2020.Apr)

user = xreg

start = 2018.Jan

data = (0.167 -0.083 0.167 0 -0.75 0 -0.167 -0.5 0.083 0.083 -0.667 0.417 0.167 -0.083 0.167 1 1.25 0 -0.167 0.5 0.083

1.083 -0.667 -0.583 0.167 0.917 0.167 0 0.25 0 0.833 0.5 0.083 -0.917 0.333 -0.583 0.167 0.917 -0.833 0 0.25 0

0.833 0.5 0.083 -0.917 0.333 -0.583 -0.833 0.917 0.167 0 0.25 0 -0.167 0.5 0.083 0.083 0.333 -0.583 0.167 -0.083

0.167 -1 0.25 0 -0.167 0.5 -0.917 0.083 0.333 -0.583 0.167 0.917 0.167 0 -0.75 0 -0.167 0.5 0.083 0.083 -0.667

-0.583)

usertype = holiday

b = (-0.009775331669 0.005672339937 -0.1206139572)

}

arima{

model = (0 1 1)(0 1 1)

ma = (0.1526222204 0.9988015939)

} X-13ARIMA-SEATSで指定できる異常値は以下の6つ。

そのうち、RP、TL、SOはマニュアルで設定する必要がある。

異常値を説明変数としない場合は以下の方法による。

# outlier.types を 'none' とする。

seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", xreg = xreg_holiday, regression.usertype = "holiday", outlier.types = "none") %>%

summary()

Call:

seas(x = iip_nsa, xreg = xreg_holiday, transform.function = "log",

x11 = "", x11.mode = "mult", regression.usertype = "holiday",

outlier.types = "none")

Coefficients:

Estimate Std. Error z value Pr(>|z|)

xreg -0.0094246 0.0047904 -1.967 0.0491 *

Weekday 0.0053744 0.0007067 7.605 0.000000000000028411 ***

AR-Nonseasonal-01 0.9045956 0.1238288 7.305 0.000000000000276832 ***

AR-Nonseasonal-02 -0.0103306 0.1472428 -0.070 0.9441

AR-Nonseasonal-03 -0.1041234 0.1122226 -0.928 0.3535

MA-Nonseasonal-01 0.9208363 0.0715228 12.875 < 0.0000000000000002 ***

MA-Seasonal-12 0.9955995 0.1226343 8.118 0.000000000000000472 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

X11 adj. ARIMA: (3 1 1)(0 1 1) Obs.: 72 Transform: log

AICc: 333.1, BIC: 346.8 QS (no seasonality in final):0.00262

Box-Ljung (no autocorr.): 37.01 * Shapiro (normality): 0.9618 *sa_x11_holiday <- seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", regression.usertype = "holiday", xreg = xreg_holiday)

sa_x11 <- seas(x = iip_nsa, x11 = "", transform.function = "log")# 祝日変数を加える場合

sa_x11_holiday$data[, "final"] Jan Feb Mar Apr May Jun Jul

2018 111.92600 114.68961 116.10976 114.52606 116.51286 114.80724 113.90585

2019 112.17400 114.03756 113.70553 112.84547 116.86861 113.37785 112.65659

2020 108.36134 105.92886 105.81370 94.84551 89.56224 89.04469 95.16746

2021 106.63680 105.72433 105.92885 108.09641 107.18578 108.39385 107.46500

2022 104.69168 105.72699 105.33594 104.74813 102.42440 104.97751 106.33672

2023 100.58587 104.09903 104.43746 104.83104 104.62112 104.84753 103.47962

Aug Sep Oct Nov Dec

2018 114.41337 112.78876 115.56996 114.35340 115.40681

2019 111.95050 112.64836 107.79167 107.59688 107.94129

2020 97.87907 99.67701 103.63844 103.93828 102.62711

2021 104.12369 98.38007 101.78868 107.11081 104.85151

2022 107.93589 107.15410 106.19052 105.74602 104.65350

2023 102.85893 103.51903 104.97694 104.10680 105.55863# 祝日変数を加えない場合

sa_x11$data[, "final"] Jan Feb Mar Apr May Jun Jul

2018 111.54134 114.65567 115.29644 114.40903 120.24186 114.75797 114.19865

2019 111.77431 114.11385 112.75360 111.77548 118.11796 113.15860 113.13099

2020 107.95239 105.00283 105.10101 94.85061 90.89392 89.11849 94.69289

2021 105.91141 105.04469 106.45463 108.09213 108.40196 108.50463 106.83711

2022 104.98321 105.14542 104.91270 104.60015 103.31046 105.11903 106.67995

2023 99.98770 104.58642 104.11551 105.56733 105.42752 104.99825 103.81013

Aug Sep Oct Nov Dec

2018 115.23537 112.30130 115.66835 114.49435 114.10219

2019 111.54635 112.31336 106.79662 107.63815 107.91572

2020 97.50479 99.45273 104.55204 103.09261 102.67633

2021 103.93563 98.08898 102.58616 106.53031 104.83871

2022 107.98039 106.79780 105.93994 105.29270 104.48759

2023 102.89955 104.06660 104.84043 103.72956 105.29618# 両者の差

sa_x11_holiday$data[, "final"] - sa_x11$data[, "final"] Jan Feb Mar Apr May

2018 0.384658442 0.033944369 0.813323809 0.117028735 -3.728999227

2019 0.399693663 -0.076296903 0.951933625 1.069986029 -1.249342180

2020 0.408949425 0.926029081 0.712696244 -0.005093748 -1.331676393

2021 0.725384728 0.679637407 -0.525773720 0.004278388 -1.216178438

2022 -0.291530010 0.581569254 0.423237848 0.147981544 -0.886062815

2023 0.598171252 -0.487389436 0.321949076 -0.736291734 -0.806403990

Jun Jul Aug Sep Oct

2018 0.049275629 -0.292801337 -0.821999678 0.487458198 -0.098390298

2019 0.219248623 -0.474402390 0.404148187 0.334996705 0.995050307

2020 -0.073794932 0.474566377 0.374278327 0.224274300 -0.913593099

2021 -0.110779312 0.627884793 0.188059747 0.291098687 -0.797481890

2022 -0.141516948 -0.343236498 -0.044495504 0.356305329 0.250586190

2023 -0.150720436 -0.330508066 -0.040613991 -0.547565987 0.136504034

Nov Dec

2018 -0.140951021 1.304618477

2019 -0.041264414 0.025569269

2020 0.845673507 -0.049221901

2021 0.580498409 0.012803716

2022 0.453317928 0.165909442

2023 0.377234830 0.262451576X11の季節変動成分移動平均項数の指定方法

seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", xreg = xreg_holiday, regression.usertype = "holiday", x11.seasonalma = "dummy")Error: X-13 run failed

Errors: - Improper value(s) entered for seasonalma. Valid choices of seasonal filter are s3x1, s3x3, s3x5, s3x9, s3x15, stable, msr, or x11default.

sa_x11_holiday_ma_default <- seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", xreg = xreg_holiday, regression.usertype = "holiday", x11.seasonalma = "x11default")summary(sa_x11_holiday_ma_default)

Call:

seas(x = iip_nsa, xreg = xreg_holiday, transform.function = "log",

x11 = "", x11.mode = "mult", regression.usertype = "holiday",

x11.seasonalma = "x11default")

Coefficients:

Estimate Std. Error z value Pr(>|z|)

xreg -0.0097753 0.0046864 -2.086 0.037 *

Weekday 0.0056723 0.0007199 7.879 0.00000000000000329 ***

LS2020.Apr -0.1206140 0.0269014 -4.484 0.00000734116067634 ***

MA-Nonseasonal-01 0.1526222 0.1069457 1.427 0.154

MA-Seasonal-12 0.9988016 0.1266074 7.889 0.00000000000000305 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

X11 adj. ARIMA: (0 1 1)(0 1 1) Obs.: 72 Transform: log

AICc: 314.8, BIC: 325.6 QS (no seasonality in final):0.03806

Box-Ljung (no autocorr.): 44.09 ** Shapiro (normality): 0.9854 sa_x11_holiday_ma_default$modelregression{

variables = (td1coef ls2020.Apr)

user = xreg

start = 2018.Jan

data = (0.167 -0.083 0.167 0 -0.75 0 -0.167 -0.5 0.083 0.083 -0.667 0.417 0.167 -0.083 0.167 1 1.25 0 -0.167 0.5 0.083

1.083 -0.667 -0.583 0.167 0.917 0.167 0 0.25 0 0.833 0.5 0.083 -0.917 0.333 -0.583 0.167 0.917 -0.833 0 0.25 0

0.833 0.5 0.083 -0.917 0.333 -0.583 -0.833 0.917 0.167 0 0.25 0 -0.167 0.5 0.083 0.083 0.333 -0.583 0.167 -0.083

0.167 -1 0.25 0 -0.167 0.5 -0.917 0.083 0.333 -0.583 0.167 0.917 0.167 0 -0.75 0 -0.167 0.5 0.083 0.083 -0.667

-0.583)

usertype = holiday

b = (-0.009775331669 0.005672339937 -0.1206139572)

}

arima{

model = (0 1 1)(0 1 1)

ma = (0.1526222204 0.9988015939)

} sa_x11_holiday_ma_default$data[, "final"] Jan Feb Mar Apr May Jun Jul

2018 111.92600 114.68961 116.10976 114.52606 116.51286 114.80724 113.90585

2019 112.17400 114.03756 113.70553 112.84547 116.86861 113.37785 112.65659

2020 108.36134 105.92886 105.81370 94.84551 89.56224 89.04469 95.16746

2021 106.63680 105.72433 105.92885 108.09641 107.18578 108.39385 107.46500

2022 104.69168 105.72699 105.33594 104.74813 102.42440 104.97751 106.33672

2023 100.58587 104.09903 104.43746 104.83104 104.62112 104.84753 103.47962

Aug Sep Oct Nov Dec

2018 114.41337 112.78876 115.56996 114.35340 115.40681

2019 111.95050 112.64836 107.79167 107.59688 107.94129

2020 97.87907 99.67701 103.63844 103.93828 102.62711

2021 104.12369 98.38007 101.78868 107.11081 104.85151

2022 107.93589 107.15410 106.19052 105.74602 104.65350

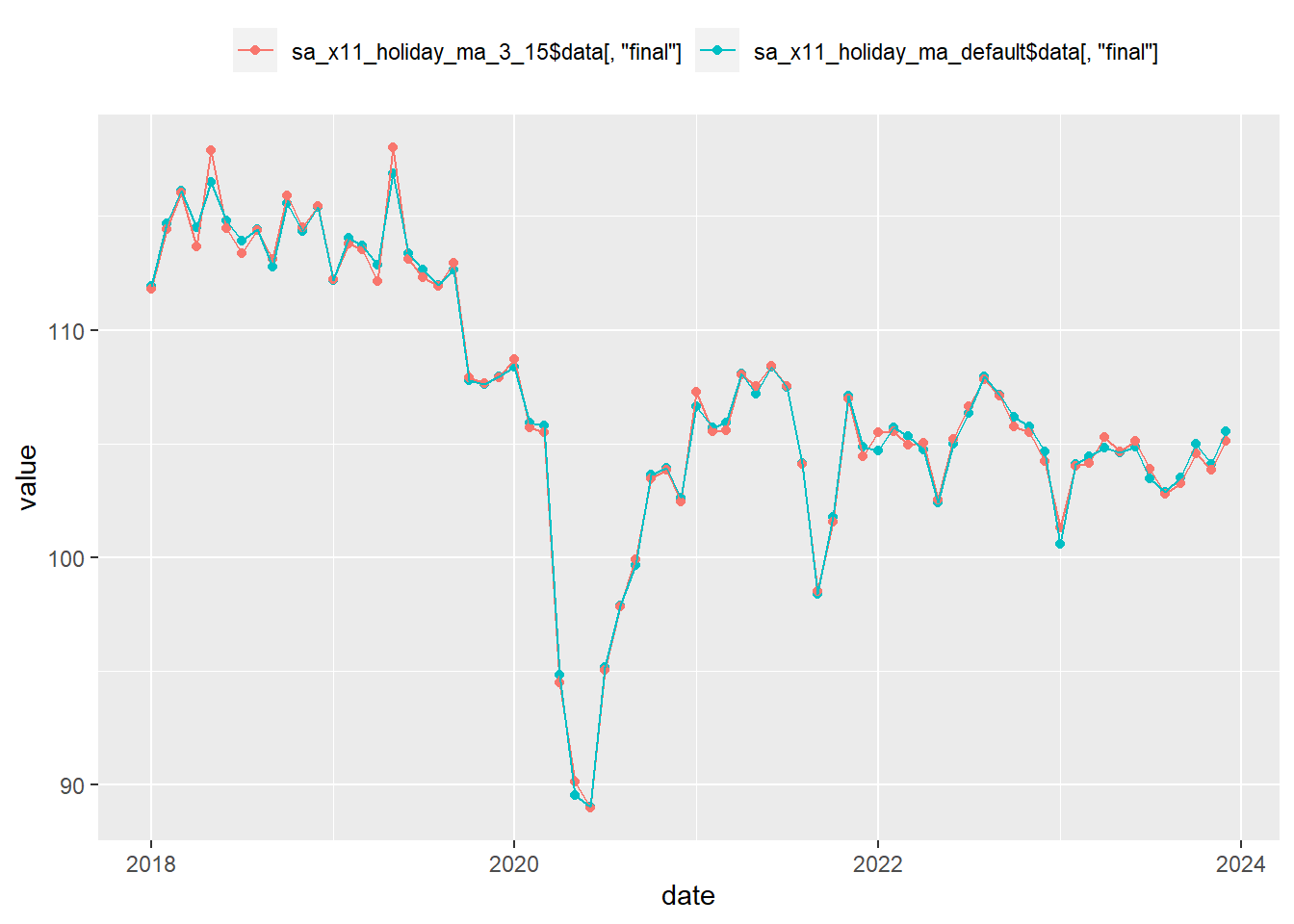

2023 102.85893 103.51903 104.97694 104.10680 105.55863sa_x11_holiday_ma_3_15 <- seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", xreg = xreg_holiday, regression.usertype = "holiday", x11.seasonalma = "s3x15")

sa_x11_holiday_ma_3_15$data[, "final"] Jan Feb Mar Apr May Jun Jul

2018 111.79621 114.41905 116.02374 113.67072 117.87946 114.46810 113.38043

2019 112.21968 113.80057 113.54598 112.12830 118.01919 113.12399 112.29168

2020 108.72605 105.71051 105.51730 94.49156 90.16128 88.99710 95.07124

2021 107.29176 105.55011 105.60227 108.04731 107.51733 108.42878 107.54626

2022 105.48447 105.55011 104.95257 105.02849 102.53118 105.22255 106.65859

2023 101.29503 104.00795 104.15344 105.27068 104.63162 105.12539 103.89080

Aug Sep Oct Nov Dec

2018 114.39723 113.12633 115.91457 114.48920 115.42858

2019 111.94549 112.94909 107.89932 107.65800 107.89409

2020 97.82959 99.93299 103.45103 103.85953 102.44996

2021 104.08967 98.49991 101.55080 106.96710 104.44389

2022 107.81958 107.09835 105.75927 105.50979 104.21368

2023 102.79228 103.26133 104.56563 103.85816 105.11779cbind(sa_x11_holiday_ma_default$data[, "final"], sa_x11_holiday_ma_3_15$data[, "final"]) %>%

{

date = as.Date(.)

data.frame(date, ., check.names = F)

} %>%

gather(key = "key", value = "value", colnames(.)[-1]) %>%

ggplot(mapping = aes(x = date, y = value, col = key)) + geom_point() + geom_line() + theme(legend.position = "top", legend.title = element_blank())

X11の趨勢循環変動成分移動平均項数の指定方法

seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", xreg = xreg_holiday, regression.usertype = "holiday", x11.seasonalma = "x11default", x11.trendma = 1000)Error: X-13 run failed

Errors: - Length of Henderson trend filter must be a positive odd integer.

seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", xreg = xreg_holiday, regression.usertype = "holiday", x11.seasonalma = "x11default", x11.trendma = 11111)Error: X-13 run failed

Errors: - Length of Henderson filter cannot exceed 101. No seasonal adjustment this run

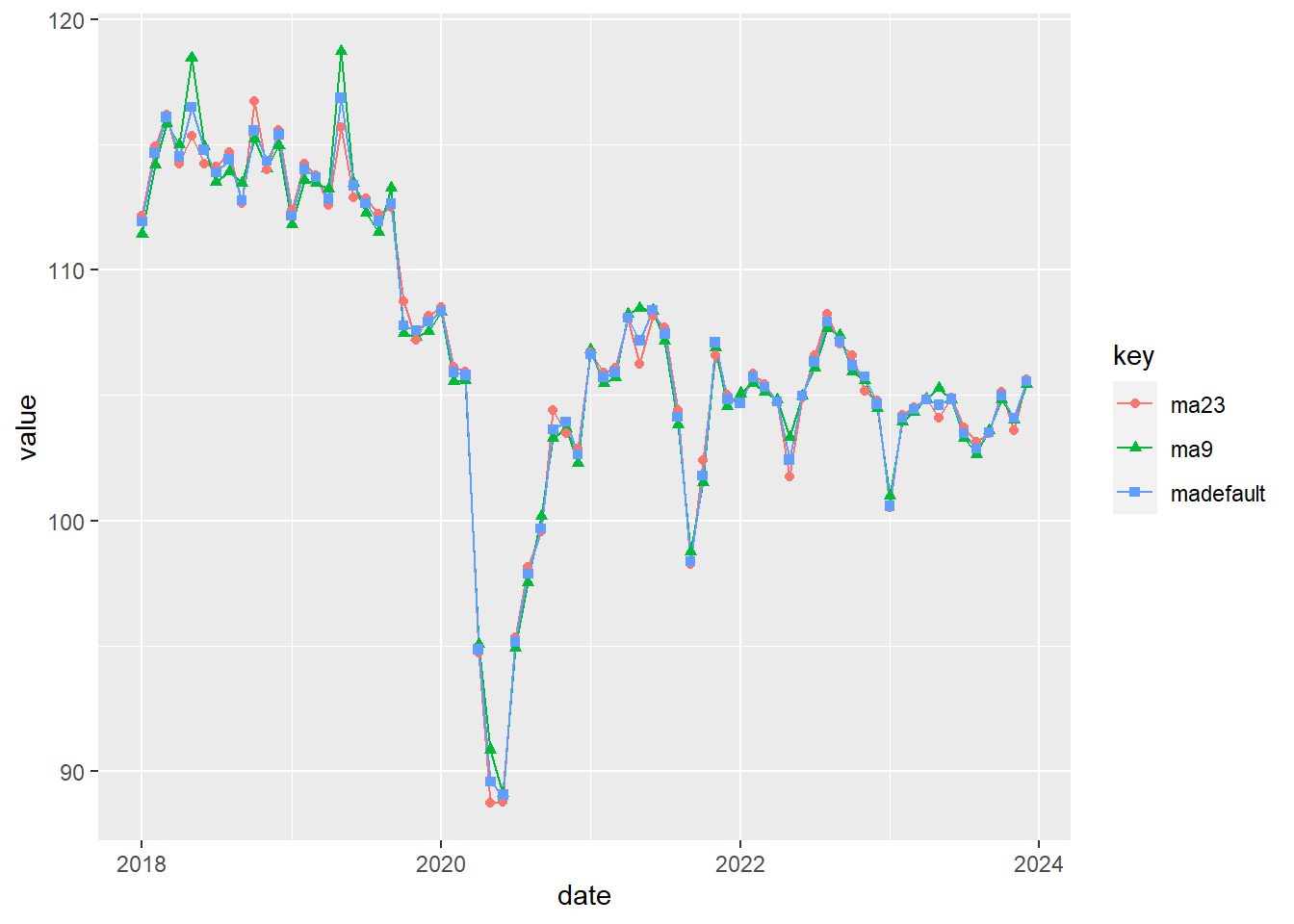

「趨勢循環変動成分をヘンダーソン加重移動平均による算出する際の移動平均項数を指定。省略時には、月次データの場合、通常は13項移動平均が適用されますが、著しく不規則変動の大きい系列には、23項移動平均を、また非常に滑らかな系列については、9項移動平均が適用されます。四半期データの場合は、5項移動平均、または7項移動平均が適用されます」

移動平均項数を9、23とした場合と指定せずにデフォルトとした場合とを比較する。

date <- df_iip$date

ma9 <- seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", xreg = xreg_holiday, regression.usertype = "holiday", x11.seasonalma = "x11default", x11.trendma = 9) %>%

{

.$data[, "final"]

}

ma23 <- seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", xreg = xreg_holiday, regression.usertype = "holiday", x11.seasonalma = "x11default", x11.trendma = 23) %>%

{

.$data[, "final"]

}

madefault <- seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", xreg = xreg_holiday, regression.usertype = "holiday", x11.seasonalma = "x11default") %>%

{

.$data[, "final"]

}

data.frame(ma9, ma23) %>%

data.frame(date, ., madefault) %>%

gather(key = "key", value = "value", colnames(.)[-1]) %>%

ggplot(mapping = aes(x = date, y = value, col = key, shape = key)) + geom_line() + geom_point()

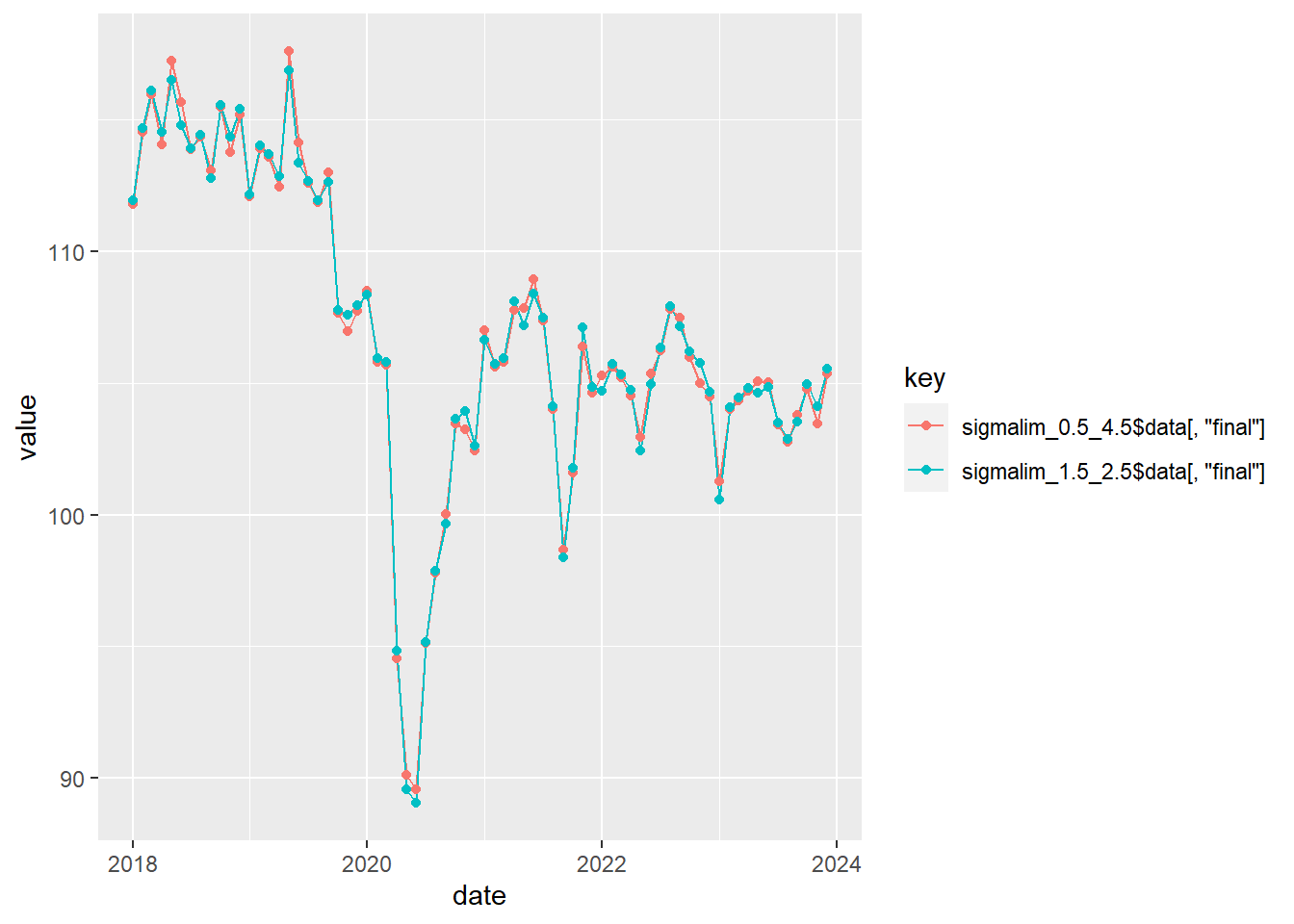

「異常値管理限界(判定基準)の上限および下限を指定。判定基準から異常値として判定された不規則変動成分に偏りの大きさに応じた修正ウエイトをかけて、「異常値調整済不規則変動成分」を算出する。省略時は、上限2.5、下限1.5が設定されます」

鉱工業指数の季節調整法の管理限界設定はデフォルト(上限2.5、下限1.5)。

sigmalim_0.5_4.5 <- seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", xreg = xreg_holiday, regression.usertype = "holiday", x11.seasonalma = "x11default", x11.sigmalim = c(0.5, 4.5)) # c(下限,上限)

sigmalim_1.5_2.5 <- seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", xreg = xreg_holiday, regression.usertype = "holiday", x11.seasonalma = "x11default", x11.sigmalim = c(1.5, 2.5))

cbind(sigmalim_0.5_4.5$data[, "final"], sigmalim_1.5_2.5$data[, "final"]) %>%

{

date = as.Date(.)

add_column(.data = data.frame(., check.names = F), date, .before = 1)

} %>%

gather(key = "key", value = "value", colnames(.)[-1]) %>%

ggplot(mapping = aes(x = date, y = value, col = key)) + geom_line() + geom_point()

指定しない場合はデフォルトが設定される。

# 指定あり

seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", xreg = xreg_holiday, regression.usertype = "holiday", x11.seasonalma = "x11default", x11.sigmalim = c(1.5, 2.5)) %>%

{

.$data[, "final"]

}

# 指定なし

seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", xreg = xreg_holiday, regression.usertype = "holiday", x11.seasonalma = "x11default") %>%

{

.$data[, "final"]

} Jan Feb Mar Apr May Jun Jul

2018 111.92600 114.68961 116.10976 114.52606 116.51286 114.80724 113.90585

2019 112.17400 114.03756 113.70553 112.84547 116.86861 113.37785 112.65659

2020 108.36134 105.92886 105.81370 94.84551 89.56224 89.04469 95.16746

2021 106.63680 105.72433 105.92885 108.09641 107.18578 108.39385 107.46500

2022 104.69168 105.72699 105.33594 104.74813 102.42440 104.97751 106.33672

2023 100.58587 104.09903 104.43746 104.83104 104.62112 104.84753 103.47962

Aug Sep Oct Nov Dec

2018 114.41337 112.78876 115.56996 114.35340 115.40681

2019 111.95050 112.64836 107.79167 107.59688 107.94129

2020 97.87907 99.67701 103.63844 103.93828 102.62711

2021 104.12369 98.38007 101.78868 107.11081 104.85151

2022 107.93589 107.15410 106.19052 105.74602 104.65350

2023 102.85893 103.51903 104.97694 104.10680 105.55863

Jan Feb Mar Apr May Jun Jul

2018 111.92600 114.68961 116.10976 114.52606 116.51286 114.80724 113.90585

2019 112.17400 114.03756 113.70553 112.84547 116.86861 113.37785 112.65659

2020 108.36134 105.92886 105.81370 94.84551 89.56224 89.04469 95.16746

2021 106.63680 105.72433 105.92885 108.09641 107.18578 108.39385 107.46500

2022 104.69168 105.72699 105.33594 104.74813 102.42440 104.97751 106.33672

2023 100.58587 104.09903 104.43746 104.83104 104.62112 104.84753 103.47962

Aug Sep Oct Nov Dec

2018 114.41337 112.78876 115.56996 114.35340 115.40681

2019 111.95050 112.64836 107.79167 107.59688 107.94129

2020 97.87907 99.67701 103.63844 103.93828 102.62711

2021 104.12369 98.38007 101.78868 107.11081 104.85151

2022 107.93589 107.15410 106.19052 105.74602 104.65350

2023 102.85893 103.51903 104.97694 104.10680 105.55863ARIMAモデルを用いて、4~5年分の予測値を推計します。原系列にこの予測値を追加した事前調整済原系列に対しX-11の移動平均を行うと、系列末端部分においても予測値を利用した中心移動平均による移動平均が可能となり、季調済系列の安定性が高まります。X-11の標準中心移動平均では、前後約7年分のデータを使用しますが、6、7年めのデータのウエイトはかなり小さいので、5年分程度のデータがあれば十分です。

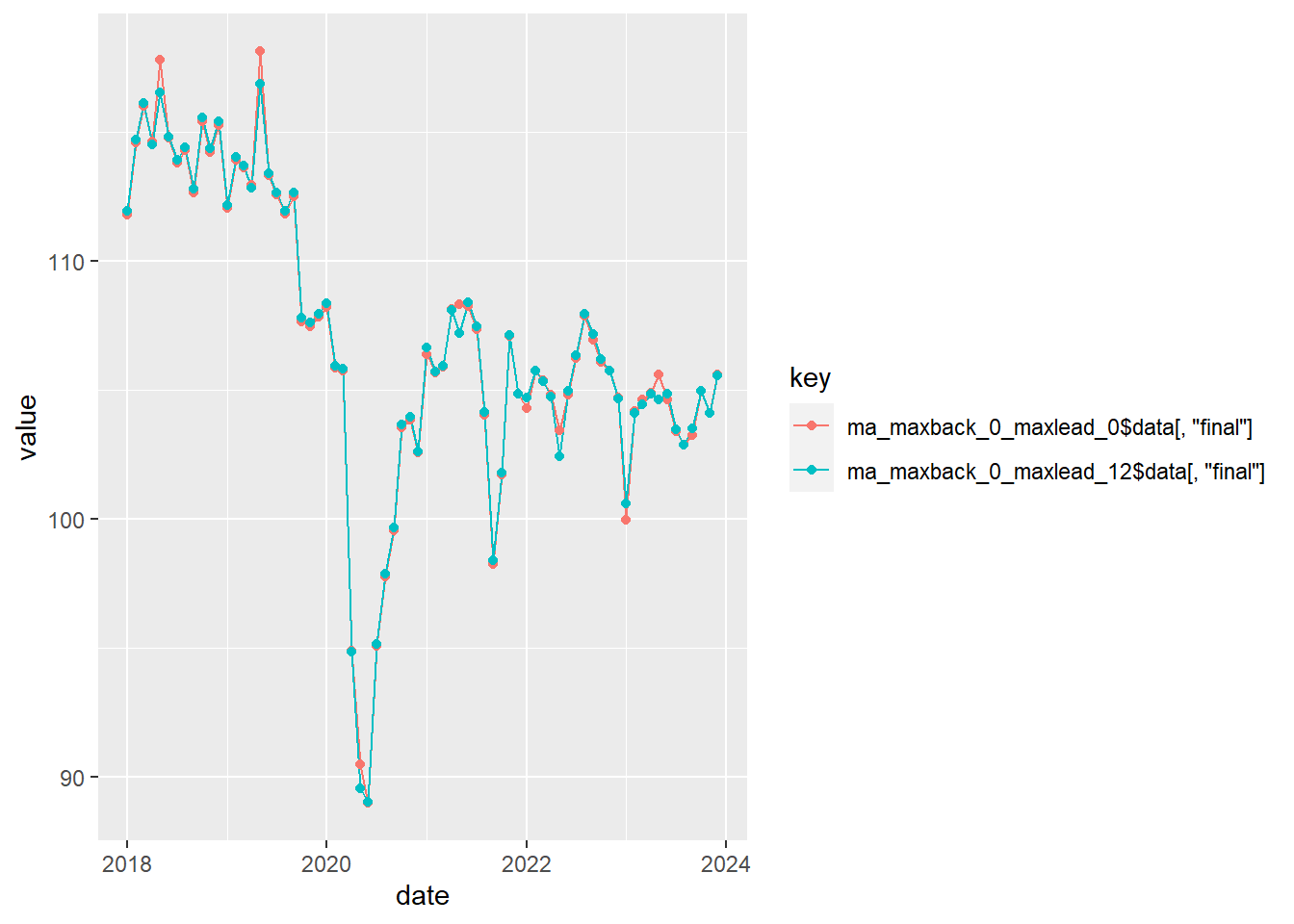

鉱工業指数の先行き予測期間は12か月、後戻り予測期間はなし。

先行き予測期間を「12か月」とした場合と「なし」とした場合を比較します。

ma_maxback_0_maxlead_12 <- seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", xreg = xreg_holiday, regression.usertype = "holiday", x11.seasonalma = "x11default", forecast.maxlead = 12, forecast.maxback = 0)

ma_maxback_0_maxlead_0 <- seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", xreg = xreg_holiday, regression.usertype = "holiday", x11.seasonalma = "x11default", forecast.maxlead = 0, forecast.maxback = 0)

cbind(ma_maxback_0_maxlead_0$data[, "final"], ma_maxback_0_maxlead_12$data[, "final"]) %>%

{

date <- as.Date(.)

add_column(.data = data.frame(., check.names = F), date, .before = 1)

} %>%

gather(key = "key", value = "value", colnames(.)[-1]) %>%

ggplot(mapping = aes(x = date, y = value, col = key)) + geom_line() + geom_point()

今回適用した祝日変数の範囲を超えているためエラーが出る。

seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", xreg = xreg_holiday, regression.usertype = "holiday", x11.seasonalma = "x11default", forecast.maxlead = 13)Error: X-13 run failed

Errors: - forecasts end date, 2025.Jan, must end on or before user-defined regression variables end date, 2024.Dec.

前回基準改定作業に則り、①(011)(011)モデルで仮外れ値を検出、②仮外れ値を変数として設定した上で、BICの小さいモデルを選ぶこととした。

平成27年基準における選択結果は、以下のとおり。

曜日はデフォルト、祝祭日はカレンダーよりユーザ型回帰変数を用い、左記のとおりRegARIMAモデルを決定。なお、うるう年が有意ではなかったため設定はしていない。異常値は、定期的(年間補正時)にoutlierコマンドによって全てのタイプの異常値を検出する。原則として検出された全ての異常値を取り入れるが、経済事象や系列の性質を考慮した上で、暫定季節指数の安定性に関する検証等を行い、異常値の検出期間の設定や、異常値のタイプ等を必要に応じて調整する。

# 鉱工業生産指数の季節調整系列

iip_sa <- df_iip$IIP_SA %>%

ts(start = df_iip$date %>%

head(1) %>%

{

c(year(.), month(.))

}, end = df_iip$date %>%

tail(1) %>%

{

c(year(.), month(.))

}, frequency = 12)

# seas {seasonal} を利用した季節調整

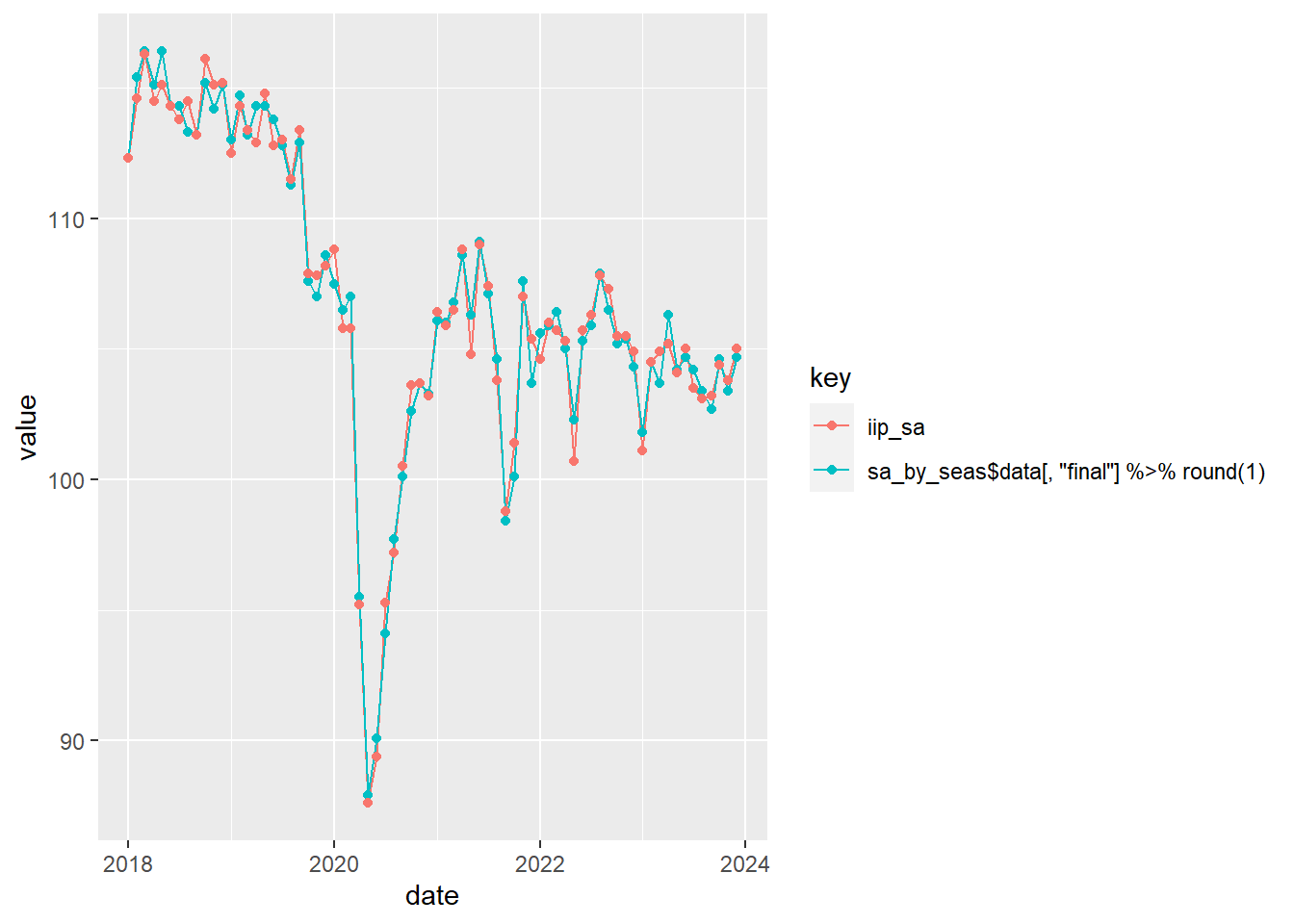

sa_by_seas <- seas(x = iip_nsa, x11 = "", transform.function = "log", x11.mode = "mult", xreg = xreg_holiday, regression.usertype = "holiday", x11.seasonalma = "x11default", forecast.maxlead = 12, forecast.maxback = 0, outlier.types = "all", regression.variables = c("td"), arima.model = "(1 1 0)(0 1 1)")

cbind(sa_by_seas$data[, "final"] %>%

round(1), iip_sa) %>%

{

date <- as.Date(.)

add_column(.data = data.frame(., check.names = F), date, .before = 1)

} %>%

gather(key = "key", value = "value", colnames(.)[-1]) %>%

ggplot(mapping = aes(x = date, y = value, col = key)) + geom_line() + geom_point()

list(sa_by_seas = sa_by_seas$data[, "final"] %>%

round(1), iip_sa = iip_sa)$sa_by_seas

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2018 112.3 115.4 116.4 115.1 116.4 114.3 114.3 113.3 113.2 115.2 114.2 115.1

2019 113.0 114.7 113.2 114.3 114.3 113.8 112.8 111.3 112.9 107.6 107.0 108.6

2020 107.5 106.5 107.0 95.5 87.9 90.1 94.1 97.7 100.1 102.6 103.7 103.3

2021 106.1 106.0 106.8 108.6 106.3 109.1 107.1 104.6 98.4 100.1 107.6 103.7

2022 105.6 105.9 106.4 105.0 102.3 105.3 105.9 107.9 106.5 105.2 105.4 104.3

2023 101.8 104.5 103.7 106.3 104.2 104.7 104.2 103.4 102.7 104.6 103.4 104.7

$iip_sa

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2018 112.3 114.6 116.3 114.5 115.1 114.3 113.8 114.5 113.2 116.1 115.1 115.2

2019 112.5 114.3 113.4 112.9 114.8 112.8 113.0 111.5 113.4 107.9 107.8 108.2

2020 108.8 105.8 105.8 95.2 87.6 89.4 95.3 97.2 100.5 103.6 103.7 103.2

2021 106.4 105.9 106.5 108.8 104.8 109.0 107.4 103.8 98.8 101.4 107.0 105.4

2022 104.6 106.0 105.7 105.3 100.7 105.7 106.3 107.8 107.3 105.5 105.5 104.9

2023 101.1 104.5 104.9 105.2 104.1 105.0 103.5 103.1 103.2 104.4 103.8 105.0sa_by_seas$modelregression{

variables = (td ls2020.Apr tc2020.May tc2021.Sep)

user = xreg

start = 2018.Jan

data = (0.167 -0.083 0.167 0 -0.75 0 -0.167 -0.5 0.083 0.083 -0.667 0.417 0.167 -0.083 0.167 1 1.25 0 -0.167 0.5 0.083

1.083 -0.667 -0.583 0.167 0.917 0.167 0 0.25 0 0.833 0.5 0.083 -0.917 0.333 -0.583 0.167 0.917 -0.833 0 0.25 0

0.833 0.5 0.083 -0.917 0.333 -0.583 -0.833 0.917 0.167 0 0.25 0 -0.167 0.5 0.083 0.083 0.333 -0.583 0.167 -0.083

0.167 -1 0.25 0 -0.167 0.5 -0.917 0.083 0.333 -0.583 0.167 0.917 0.167 0 -0.75 0 -0.167 0.5 0.083 0.083 -0.667

-0.583)

usertype = holiday

b = (-0.007691896234 0.004779864019 -0.002075744234 0.01062036089 0.0008772311586 0.01495507019 -0.01599901823

-0.1043061562 -0.1011703923 -0.08235363489)

}

arima{

model = (1 1 0)(0 1 1)

ar = -0.4281277311

ma = 0.9289627598

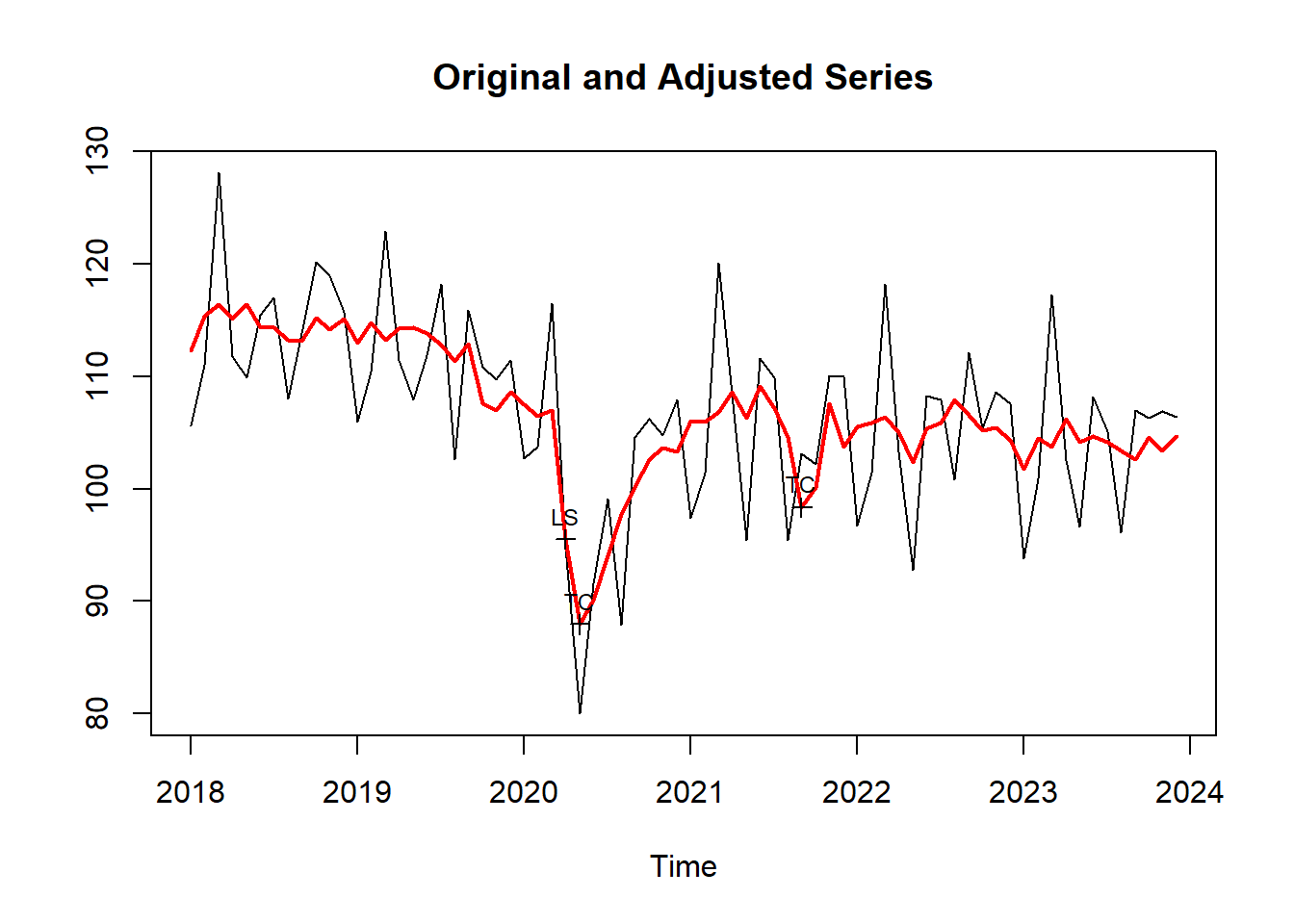

} sa_by_seas %>%

summary()

Call:

seas(x = iip_nsa, xreg = xreg_holiday, transform.function = "log",

x11 = "", x11.mode = "mult", regression.usertype = "holiday",

x11.seasonalma = "x11default", forecast.maxlead = 12, forecast.maxback = 0,

outlier.types = "all", regression.variables = c("td"), arima.model = "(1 1 0)(0 1 1)")

Coefficients:

Estimate Std. Error z value Pr(>|z|)

xreg -0.0076919 0.0039438 -1.950 0.051131 .

Mon 0.0047799 0.0051845 0.922 0.356551

Tue -0.0020757 0.0049689 -0.418 0.676134

Wed 0.0106204 0.0049943 2.126 0.033463 *

Thu 0.0008772 0.0049518 0.177 0.859388

Fri 0.0149551 0.0048368 3.092 0.001989 **

Sat -0.0159990 0.0045031 -3.553 0.000381 ***

LS2020.Apr -0.1043062 0.0214225 -4.869 0.00000112 ***

TC2020.May -0.1011704 0.0211747 -4.778 0.00000177 ***

TC2021.Sep -0.0823536 0.0194004 -4.245 0.00002187 ***

AR-Nonseasonal-01 -0.4281277 0.1019111 -4.201 0.00002657 ***

MA-Seasonal-12 0.9289628 0.1107758 8.386 < 0.0000000000000002 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

X11 adj. ARIMA: (1 1 0)(0 1 1) Obs.: 72 Transform: log

AICc: 302.1, BIC: 321 QS (no seasonality in final):0.1736

Box-Ljung (no autocorr.): 24.31 Shapiro (normality): 0.9815 plot(sa_by_seas)

Sys.time()[1] "2024-04-09 15:09:01 JST"R.Version()$version.string[1] "R version 4.3.3 (2024-02-29 ucrt)"quarto::quarto_version()[1] '1.4.542'packageVersion(pkg = "tidyverse")[1] '2.0.0'