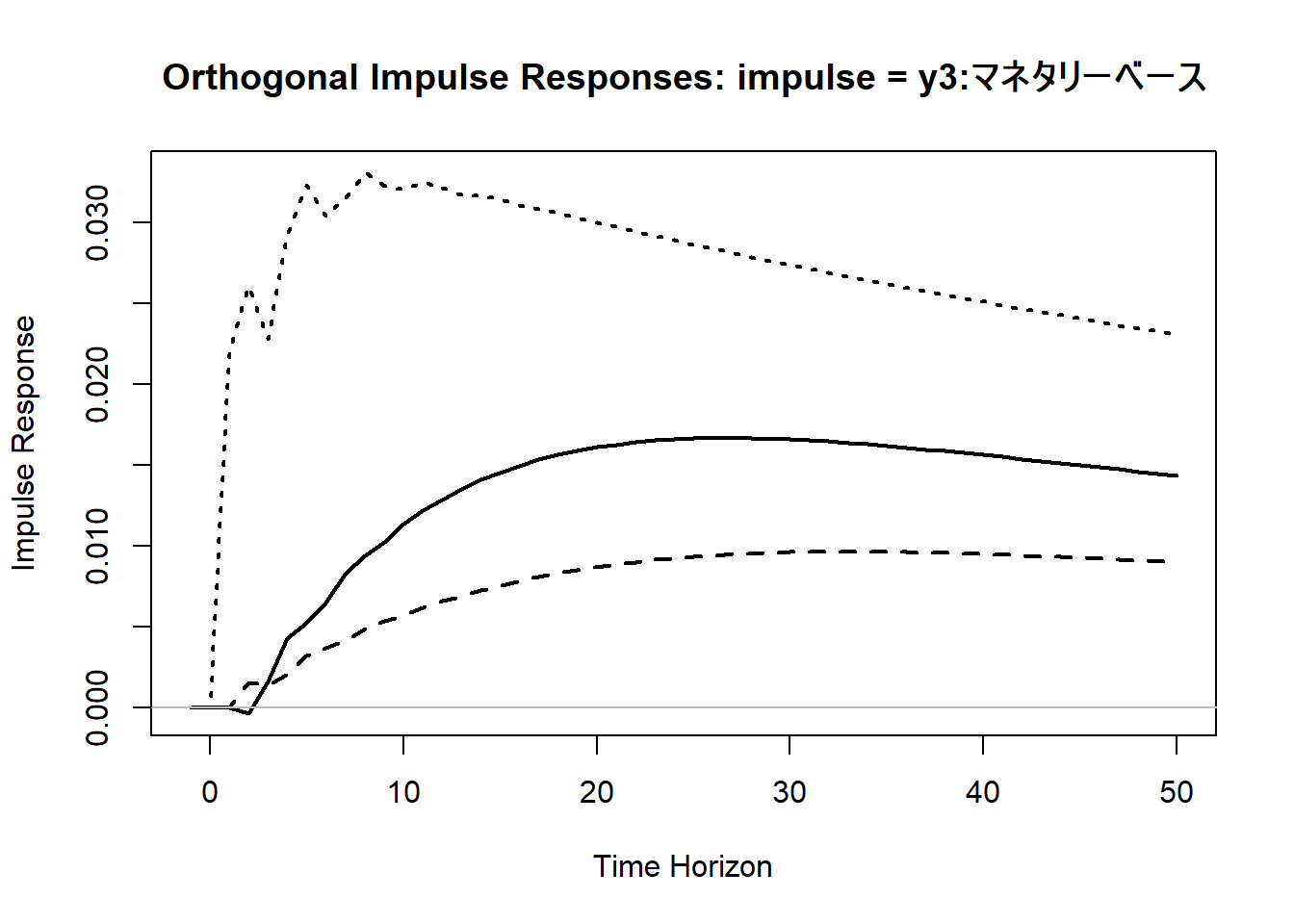

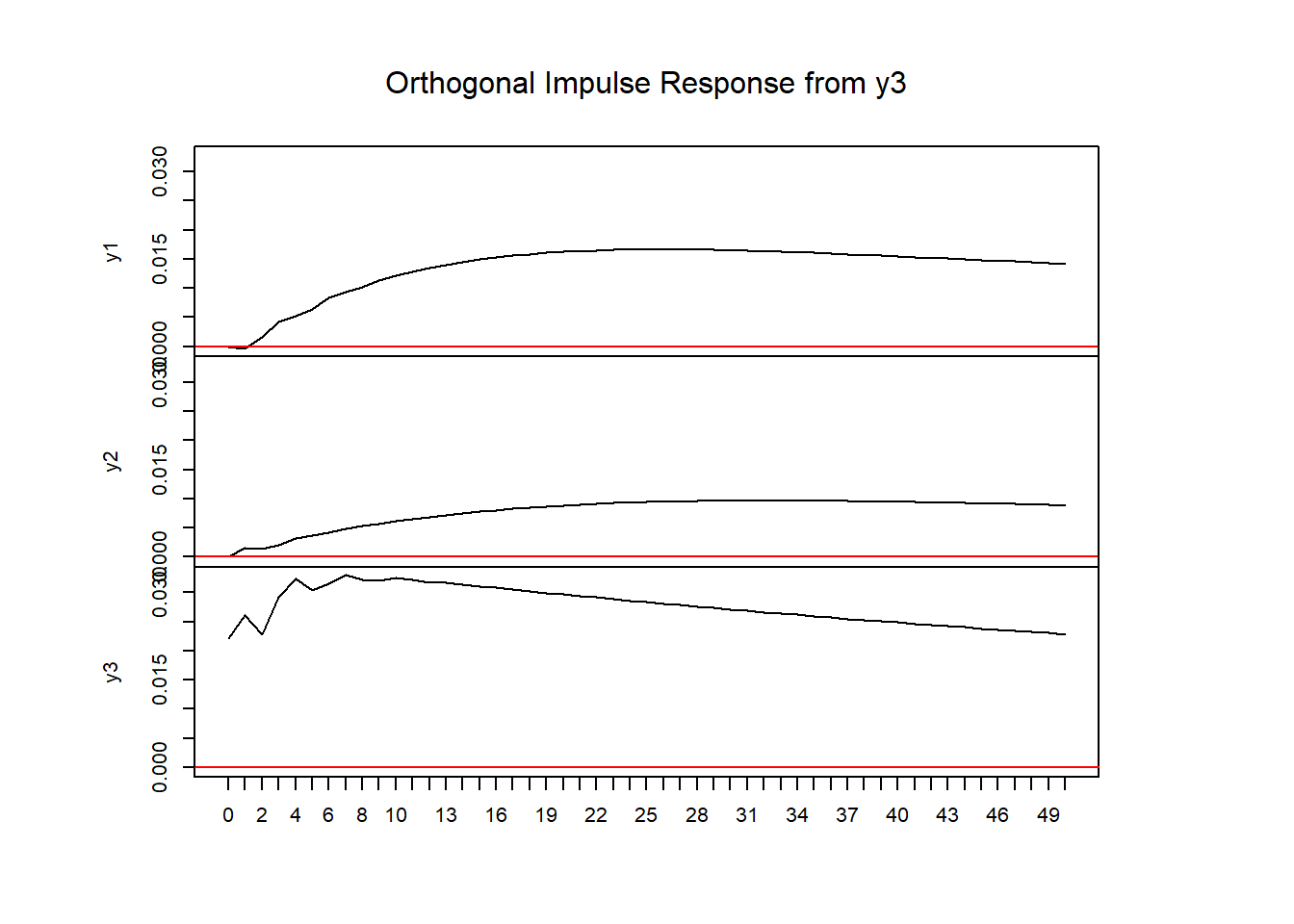

インパルス応答分析のアルゴリズム

時点\(\,h=0\,\)において、構造VARモデルの撹乱項に定数値からなる\(\,K\times1\,\)のベクトル\(\,\delta\,\)が発生したとする。

このとき、ショック\(\,\delta\,\)の内生変数\(\,\textbf{y}_t\,\)への波及(限界)効果(内生変数\(\,\textbf{y}\,\)の変化分)をインパルス応答値\(\,\Delta\textbf{y}\,\)と呼び、その動的変化を調べることがインパルス応答分析である。

前述の通り構造VARモデルの\(\,h=0\,\)時点に外生的なショック\(\,\pmb{\delta}\,\)が撹乱項を通じて同モデルに伝わった場合、インパルス応答値\(\,\Delta\textbf{y}\,\)は以下のように変化する。

|

時点

|

インパルス応答値

|

|

\(t=-1\)

|

\(\Delta\textbf{y}_{-1}=0\)

|

|

\(t=0\)

|

\(\textbf{A}\Delta\textbf{y}_0=\pmb{\delta}\)

|

|

\(t=1\)

|

\(\textbf{A}\Delta\textbf{y}_1=\textbf{A}_1\Delta\textbf{y}_0\)

|

|

\(t=2\)

|

\(\textbf{A}\Delta\textbf{y}_2=\textbf{A}_1\Delta\textbf{y}_1+\textbf{A}_2\Delta\textbf{y}_0\)

|

|

\(t=3\)

|

\(\textbf{A}\Delta\textbf{y}_3=\textbf{A}_1\Delta\textbf{y}_2+\textbf{A}_2\Delta\textbf{y}_1\)

|

|

\(\vdots\)

|

\(\vdots\)

|

|

\(t=h\)

|

\(\textbf{A}\Delta\textbf{y}_h=\textbf{A}_1\Delta\textbf{y}_{h-1}+\textbf{A}_2\Delta\textbf{y}_{h-2}\)

|

上表を誘導VARモデルの視点に直すと、

|

時点

|

インパルス応答値

|

|

\(t=-1\)

|

\(\Delta\textbf{y}_{-1}=0\)

|

|

\(t=0\)

|

\(\Delta\textbf{y}_0=\textbf{A}^{-1}\pmb{\delta}\)

|

|

\(t=1\)

|

\(\Delta\textbf{y}_1=\textbf{A}^{-1}\textbf{A}_1\Delta\textbf{y}_0=\textbf{B}_1\Delta\textbf{y}_0\)

|

|

\(t=2\)

|

\(\Delta\textbf{y}_2=\textbf{A}^{-1}\textbf{A}_1\Delta\textbf{y}_1+\textbf{A}^{-1}\textbf{A}_2\Delta\textbf{y}_0=\textbf{B}_1\Delta\textbf{y}_1+\textbf{B}_2\Delta\textbf{y}_0\)

|

|

\(t=3\)

|

\(\Delta\textbf{y}_3=\textbf{A}^{-1}\textbf{A}_1\Delta\textbf{y}_2+\textbf{A}^{-1}\textbf{A}_2\Delta\textbf{y}_1=\textbf{B}_1\Delta\textbf{y}_2+\textbf{B}_2\Delta\textbf{y}_1\)

|

|

\(\vdots\)

|

\(\vdots\)

|

|

\(t=h\)

|

\(\Delta\textbf{y}_h=\textbf{A}^{-1}\textbf{A}_1\Delta\textbf{y}_{h-1}+\textbf{A}^{-1}\textbf{A}_2\Delta\textbf{y}_{h-2}=\textbf{B}_1\Delta\textbf{y}_{h-1}+\textbf{B}_2\Delta\textbf{y}_{h-2}\)

|

と表され、これは\(\,\textbf{A}^{-1}\pmb{\delta}\,\)で表現されるショックを\(\,t=0\,\)時点の誘導VARモデルに与え、上表の時点の順に逐次的にインパルス応答値を求めることは、構造VARモデルに基づくインパルス応答値を求めている事と同じである事を表している。

そこで次に\(\,\textbf{A}^{-1}\pmb{\delta}\,\)で表現される誘導VARモデルへのショックを決めることになる。

\(K\times K\,\)の対称な正値定符号行列\(\,\textbf{Q}\,\)はコレスキー分解により\[\textbf{Q}=\textbf{P}\textbf{P}^{'}\]を満たすユニークな下三角行列に分解され、修正コレスキー分解により\(\,\textbf{L}\,\)を対角要素が1の下三角行列、\(\,\textbf{D}\,\)を正の要素を持つ対角行列として\[\textbf{Q}=\textbf{L}\textbf{D}\textbf{L}^{'}\]と分解できる。

ここで、\[\textbf{L}\textbf{D}^{1/2}\left(\textbf{L}\textbf{D}^{1/2}\right)^{'}=\textbf{L}\textbf{D}^{1/2}\left(\textbf{D}^{1/2}\right)^{'}\textbf{L}^{'}=\textbf{L}\textbf{D}^{1/2}\textbf{D}^{1/2}\textbf{L}^{'}=\textbf{L}\textbf{D}\textbf{L}^{'}=\textbf{Q}=\textbf{P}\textbf{P}^{'}\]であること、かつ\(\,\textbf{P}\,\)は一意であることから\[\textbf{P}=\textbf{L}\textbf{D}^{1/2}\]となる。

前述のコレスキー分解、修正コレスキー分解を誘導撹乱項\(\,\textbf{u}_t\,\)の共分散行列\(\,\pmb{\Sigma}_u\)に適用すると\[\pmb{\Sigma}_u=\textbf{P}\textbf{P}^{'}=\textbf{L}\textbf{D}\textbf{L}^{'}\]となるが、2つの撹乱項ベクトルの通り、

\[\pmb{\Sigma}_u=\textbf{A}^{-1}\pmb{\Sigma}_\epsilon\left(\textbf{A}^{-1}\right)^{'}\] であり、 \[\pmb{\Sigma}_u=\textbf{L}\textbf{D}\textbf{L}^{'}\]でもあるため、\(\,\textbf{A}^{-1}=\textbf{L}\,\)と制約した場合、\(\,\pmb{\Sigma}_\epsilon=\textbf{D}\,\)となり、 \[\textbf{P}=\textbf{LD}^{1/2}=\textbf{A}^{-1}\textbf{D}^{1/2}=\textbf{A}^{-1}\pmb{\Sigma}_{\epsilon}^{1/2}=\textbf{A}^{-1}\pmb{\delta}\]となる。

さらに\(\,\textbf{D}\,\)の対角要素は全て正であるため、\(\textbf{D}^{1/2}=\textrm{diag}\left(\sqrt{d_1},\sqrt{d_2},\cdots,\sqrt{d_N}\right)\)となり、つまり\(\,\textbf{P}\,\)は、

- 修正コレスキー分解\(\,\pmb{\Sigma}_u=\textbf{LDL}^{-1}\,\)を利用して求めた\(\,\textbf{L}\,\)に設けた \(\,\textbf{A}^{-1}=\textbf{L}\,\)の制約の下では、対角要素が1である下三角行列\(\,\textbf{L}\,\)に、構造撹乱項\(\,\pmb{\epsilon}_t\,\)の分散の平方根である標準偏差を対角要素とする対角行列を乗じた、構造撹乱項の標準偏差を対角要素とする下三角行列となり、再帰的構造VARを構成し、

- コレスキー分解\(\,\pmb{\sum}_u=\textbf{PP}^{'}\,\)で求めた誘導撹乱項の共分散行列\(\,\pmb{\sum}_u\,\)の対角要素の平方根である\(\,\textbf{u}\,\)の標準偏差を対角要素とする下三角行列となり、ショックである\(\,\textbf{A}^{-1}\pmb{\delta}\,\)に下三角行列\(\,\textbf{P}\,\)の制約を設けたのが直交化インパルス応答といえる。

続いて期待値、分散を以下の通りに設定する標準化構造撹乱項\(\,\pmb{\epsilon}_t^{\textrm{SD}}\,\)を考える。

\[\textrm{E}\left(\pmb{\epsilon}_t^{\textrm{SD}}\right)=0,\quad\textrm{Var}\left(\pmb{\epsilon}_t^{\textrm{SD}}\right)=\textrm{E}\left[\pmb{\epsilon}_t^{\textrm{SD}}\left(\pmb{\epsilon}_t^{\textrm{SD}}\right)^{'}\right]=\textbf{I}_K,\quad \pmb{\epsilon}_t=\textbf{D}^{1/2}\pmb{\epsilon}_t^{\textrm{SD}}\]

ここで、\(\,\pmb{\epsilon}_t^{\textrm{SD}}\,\)は\(\,K\times 1\,\)のベクトルである。

\(\textbf{u}_t\)を標準化構造撹乱項\(\,\pmb{\epsilon}_t^{\textrm{SD}}\,\)で表現すると、

\[

\begin{split}

\textbf{u}_t&=\textbf{A}^{-1}\pmb{\epsilon}_t\\

&=\textbf{A}^{-1}\textbf{D}^{1/2}\pmb{\epsilon}_t^{\textrm{SD}}\\

&=\textbf{L}\textbf{D}^{1/2}\pmb{\epsilon}_t^{\textrm{SD}}\\

&=\textbf{P}\pmb{\epsilon}_t^{\textrm{SD}}

\end{split}

\] となる。

外生的なショックは1つの内生変数の撹乱項のみに1期だけ発生する想定とする。つまり、\(\,\pmb{\epsilon}_t^{\textrm{SD}}\,\)における\(\,j\,\)番目の要素\(\,\pmb{\epsilon}_{jt}^{\textrm{SD}}=1\,\)と設定し、その他の要素は\(\,0\,\)に設定する。

そのために、\(j\)番目の要素を\(\,1\,\)、他の要素を\(\,0\,\)とする\(\,K\times 1\,\)の選択ベクトル\(\,\textbf{e}_j\,\)を利用する。内生変数が3つ\(\,K=3\,\)の場合は、\(\,\textbf{e}_1=(1,0,0)^{'},\quad\textbf{e}_3=(0,0,1)^{'}\)となる。

単位ショック\(\,\pmb{\epsilon}_{jt}^{\textrm{SD}}=1\,\)の設定は

\[\textbf{P}\pmb{\epsilon}_{jt}^{\textrm{SD}}=\textbf{Pe}_j\]と表現でき、結論として誘導VARモデルには\(\,\textbf{u}_t=\textbf{Pe}_j\,\)のショックを与えることになる。